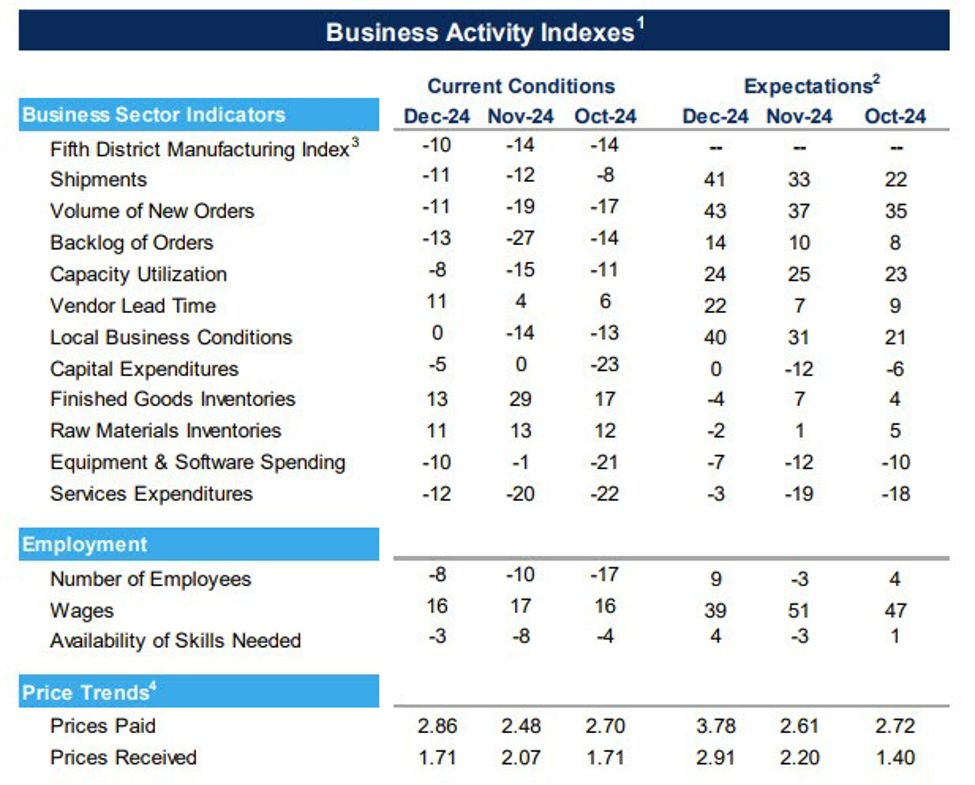

- Manufacturing Exercise: Remained in contractionary territory; composite index rose to -10 in December (from -14 in November). Est. -10

- Part Indexes:

- Shipments: -11 vs -12 final month

- Employment: -8 vs -10 final month

- New Orders: Improved to -11 vs -19 final month

- Native Enterprise Situations: Index improved to 0 (from -14); future native enterprise circumstances elevated to 40 (from 31).

- Future Expectations: Future indexes for shipments and new orders moved additional into constructive territory, signaling anticipated enhancements within the subsequent six months.

- Six-month ahead Shipments 41 versus 33

- Six-month ahead new orders 43 versus 37 final month

- Vendor Lead Time: Index elevated to 11 (from 4).

- Backlogs: Fewer corporations reported lowering backlogs; index improved to -13 (from -27).

- Costs:

- Costs Paid: 2.86 versus 2.48 final month. Progress fee elevated barely.

- Costs Acquired: 1.71 versus 2.07 final month. Progress fee decreased.

- 12-Month Expectations: Companies anticipated progress in each costs paid and costs acquired. Costs paid 3.78 versus 2.61 final month. Costs acquired 2491 versus 2.20 final month

Abstract:

The info reveals slight enhancements in present manufacturing circumstances, with lowered contractions in a number of key indicators akin to new orders, backlogs, and capability utilization. Native enterprise circumstances improved considerably, whereas vendor lead occasions elevated. Wanting ahead, expectations for the subsequent six months recommend optimism, with enhancements in shipments, new orders, and employment. Nevertheless, corporations anticipate greater value progress for each inputs and outputs.

{kind=link}