(Bloomberg) — A former hedge fund supervisor whose agency made billions through the international monetary disaster is able to pounce on volatility once more, as he sees threats to market stability at a degree not seen since 2008.

Most Learn from Bloomberg

Steve Diggle’s household workplace Vulpes Funding Administration is in search of as much as $250 million from traders as early as within the first quarter, the Oxford, UK-based investor stated in a phone interview.

Diggle, whose agency made $3 billion between 2007 and 2008, is elevating the cash for a hedge fund and managed accounts designed to generate hefty returns in market crashes and revenue from wagers on rising and falling shares in calmer intervals.

The thought to start out the brand new fund happened after the agency developed a mannequin to make use of synthetic intelligence to learn massive volumes of public info. It helped spot Asia-Pacific firms with excessive chance of blowups, on account of dangerous habits equivalent to excessive leverage, asset-liability mismatch and even outright fraud, Diggle stated. The fairness portfolio will even have single shares or indexes as bullish wagers.

Diggle is making his largest push into volatility buying and selling, after the March 2011 closure of his predecessor agency Artradis Fund Administration Pte. The then Singapore-based hedge fund agency noticed property swell to almost $5 billion in 2008, bolstered by earnings from bets on market routs and financial institution troubles, solely to later fall sufferer to a flip in markets introduced on by unprecedented central financial institution intervention.

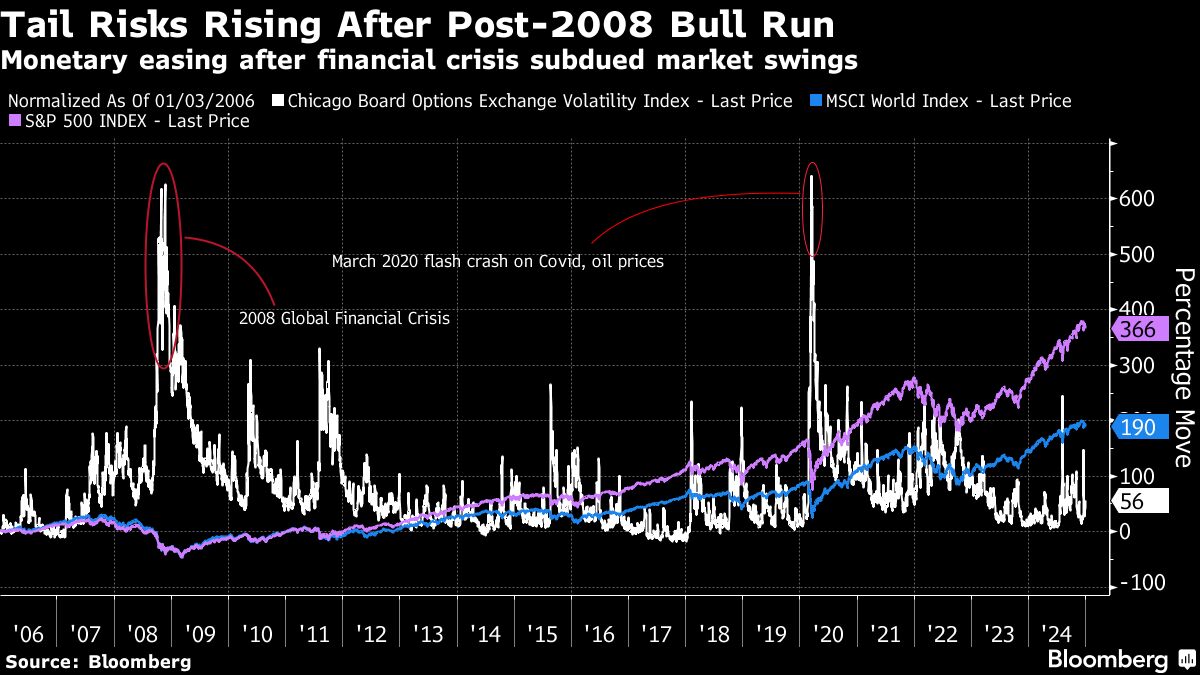

“The variety of fault strains on the market at this time are larger, and the probabilities of one thing going unsuitable are considerably larger, however danger costs have come down,” Diggle stated, drawing comparability with situations underneath greater than a decade of simple financial insurance policies. “So we’re sort of in an identical scenario to the place we had been in 2005 to 2007.”

Among the many potential flash factors are the stretched valuations of US shares, the nation’s prime workplace market glut, elevated federal debt and tight credit score spreads. A brand new “bull market technology” of merchants who entered the business after 2008 have pushed a small group of US know-how shares and crypto to dizzying heights, Diggle stated. In the meantime, it’s cheaper to purchase devices to guard in opposition to routs, he added.

Elsewhere, he cited mounting geopolitical tensions and China’s shadow banking woes. Retail punters, the rising may of passive funding funds and excessive frequency merchants will possible exacerbate routs, like they did in March 2020 and August 2024, Vulpes stated in a advertising and marketing doc for the brand new fund.

{kind=link}