What a distinction a month makes… Again in early April, shares have been crashing right into a bear market on fears that President Trump’s “Liberation Day” tariffs would freeze world commerce, reignite inflation, and ship the economic system spiraling right into a recession. After April 2’s tariff blitz, shares fell 10% in two days; one thing that’s occurred solely a handful of instances previously 100 years.

Since then – because of tariff rollbacks, resuming commerce flows, and a restabilized world economic system – the market has staged one in all its sharpest short-term rallies ever because the S&P 500 climbed almost 20% in simply over 20 days.

This rally is exhibiting no indicators of fatigue simply but… and we don’t suppose it is going to anytime quickly.

Simply look to yesterday’s Shopper Worth Index (CPI) report. In our view, it wasn’t only a “good” inflation report – it was the type of knowledge that ought to assist set the stage for an enormous summer season inventory rally.

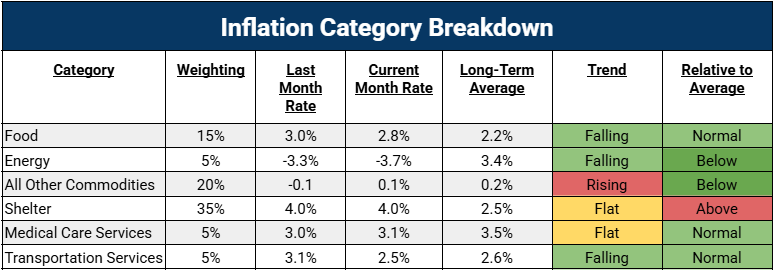

Headline CPI got here in at simply 0.2% month-over-month, beneath the 0.3% consensus. It was the identical story for core CPI – a measly 0.2% enhance, additionally undercutting estimates. Practically each main element of the index both cooled or dropped outright:

- Meals value inflation – down from 3.0% to 2.8% year-over-year

- Power inflation – nonetheless unfavourable and getting much more so, falling from -3.3% to -3.7%

- Transportation providers inflation – down from 3.1% to 2.5%.

Shelter stayed elevated; however even there, cracks are beginning to present.

In brief, inflation didn’t flare up as so many feared. It fizzled. And on this atmosphere, that’s about as bullish a signal as it gets.

However right here’s the actual kicker: April’s delicate inflation print wasn’t only a signal of easing value pressures. To us, it was a dying knell for what had been the market’s greatest concern this spring: tariff-driven reinflation.

Overblown Inflation Fears Are within the Rearview

After Trump launched the largest tariff barrage because the Smoot-Hawley days on April 4, pundits rang the alarm bells, warning of imminent value spikes.

However it appears the information is giving these doomsayers the chilly shoulder.

In March, earlier than the tariffs started, CPI inflation was 2.4%. In April – post-“Liberation Day” – it ran at 2.3%. And proper now, in keeping with the Cleveland Fed’s Nowcasting, real-time knowledge for Might is monitoring at 2.4%. It appears there’s no tariff reinflation to be seen.

How about core CPI inflation? 2.8% in March, 2.8% in April, monitoring for two.8% once more in Might – that’s a textbook definition of secure.

So, what provides? Didn’t Trump simply slap a 125% tariff on Chinese language imports, amongst different issues?

Sure; however he additionally hit the brakes.

Since “Liberation Day,” we’ve had a 90-day tariff pause, exemptions for auto components and electronics, a U.S.-UK commerce deal, and a U.S.-China commerce truce. Collectively, these actions slashed the common efficient U.S. tariff charge from a sky-high 30% to a far-more-manageable 13%.

So, if 30% tariffs didn’t spark reinflation, 13% tariffs positively shouldn’t.

That’s why we’re burying the reinflation narrative. The information is making it clear that tariffs aren’t inflicting reinflation.

And as long as issues maintain trending within the path they’re going proper now, tariffs received’t trigger any reinflation anytime quickly.

Inflation Eases, Tariffs Fall, and the Bull Market Case Will get Stronger

With that crippling concern within the rearview, there’s little left to cease this rally…

As a result of let’s take a look at the macro mosaic now:

- Inflation is secure and trending decrease: headline inflation slowed to 2.3% year-over-year in April, down from 2.4% in March.

- Tariffs are falling: U.S. tariffs on Chinese language items dropped from 145% to 30%, and Chinese language tariffs on U.S. items fell from 125% to 10%.

- Commerce offers are taking place: The U.S. and U.Ok. finalized a commerce settlement specializing in safety cooperation, and the U.S. and China signed an preliminary commerce deal decreasing tariffs and aiming to finish retaliation.

- The Federal Reserve is poised to chop charges: Policymakers anticipate two charge cuts in 2025, with the federal funds charge presently at 4.25%–4.50%

- Shopper spending is holding up: Financial institution of America knowledge signifies shopper spending grew at a 1.6% annualized charge in April 2025, exhibiting average momentum.

- Company earnings are stable: Analysts venture S&P 500 earnings development charges of 6.4% to eight.8% for Q2 by means of This fall 2025, with a full-year development estimate of 9.7%.

- AI stocks are ripping larger. In the present day, Wednesday, Might 14:

- Nvidia‘s (NVDA) shares rose 3% in premarket buying and selling after a major AI chip deal, pushing its market cap above $3 trillion.

- AMD‘s (AMD) inventory surged 5.5% following a $6 billion buyback announcement and a $10 billion three way partnership with Saudi-backed agency Humain.

- Palantir (PLTR) shares hit all-time highs, climbing 2% premarket after an 8% achieve, pushed by optimism round AI and tariff reduction.

Put all of it collectively, and we have what we call a ‘no-brainer bull market’ setup.

The Ultimate Phrase: Delicate CPI Clears the Manner for a Summer season Surge

The market’s technicals are simply as bullish because the macro backdrop is.

The S&P 500 is up 17% in simply 23 buying and selling classes. That’s occurred solely seven instances since WWII. Each single time, it marked the starting of a significant bull market.

That is what late 1998, spring 2009, and summer season 2020 felt like. When you knew what was coming then, you have been backing up the truck.

And we predict that’s precisely what buyers ought to be doing proper now…

Particularly in AI shares.

These are the businesses that can profit most from this macro tailwind cocktail of easing inflation, falling tariffs, and incoming charge cuts.

So, sure, April’s CPI report was an enormous deal. It eliminated the ultimate main roadblock to a full-fledged summer season meltup.

The rally is actual. The trail is evident, and the gasoline is loaded.

It’s time to lean in and seize ahold of the beneficial properties forward.

And we anticipate that on this summertime surge, a brand new type of AI – one thing we name AI 2.0 – will steal the highlight and rake within the greatest income on Wall Road by far.

AI 2.0 isn’t about quicker chatbots or higher spreadsheets.

It’s about bringing intelligence into our houses, our factories, our streets. It’s about machines that see, suppose, and transfer – and the businesses that flip that means into critical income.

Whereas the world’s distracted with what AI has finished… The sensible buyers are already what it’s about to do subsequent.

Learn more about some of our favorite AI 2.0 picks right now.

Questions or feedback about this difficulty? Drop us a line at langofeedback@investorplace.com.

{kind=link}