Good morning. On Friday, the Could jobs report got here in significantly better than feared. The US personal sector added 139,000 jobs and the unemployment price held regular at 4.2 per cent. There have been smooth spots, together with downward revisions for March and April. However broadly talking, this was a superb report. The US inventory market permitted, rising 1 per cent on Friday. The Fed seems set to carry charges regular for some time longer — regardless of the president’s calls for. E mail us: unhedged@ft.com.

Tesla

Everybody noticed it coming. When Donald Trump and Elon Musk made their pact forward of the 2024 election, it was extensively assumed that the partnership could be shortlived. However this was even shorter than we anticipated. And the break-up was a spectacle.

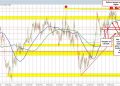

That spectacle undid a lot of the enhance Tesla inventory acquired from Musk saying that he would step again from his authorities work and deal with enterprise. Since Musk’s late April announcement, Tesla had risen almost 45 per cent. On Thursday, throughout the mud-throwing contest, the shares went down 14 per cent, and solely gained again a bit on Friday. Apparently, that fall leaves Tesla’s shares basically flat since 2022. Right here’s the chart:

Tesla shouldn’t be a inventory that — the best way to put this? — responds a lot to fundamentals. Whereas it was already down for 2025, even that fall could have been understating the numerous troubles on the automaker. Gross sales have been plummeting within the US and overseas, as Musk’s private model has turned off patrons and because the firm has misplaced floor to different EV makers, significantly low cost Chinese language opponents. Analysts had already been steadily downgrading anticipated gross sales over the previous three years, and at the moment are predicting a steeper decline on the finish of this 12 months and in 2026:

Its gross revenue margins have eroded as volumes have fallen, and they’re anticipated to go decrease nonetheless. And the opposite elements of its enterprise have had main obstacles: its higher-margin battery enterprise has been disrupted by tariffs, whereas its robotaxi fleet is falling behind opponents like Waymo.

However that brings us to the massive query. What does the massive drop final Thursday imply? What’s the market considering, because it had been?

Now we have three (not mutually unique) theories. The primary is that the market is reacting to the provisions of Trump’s huge stunning invoice. A bearish JPMorgan observe making the rounds means that the invoice may lower Tesla’s working earnings in half. They estimate a $1.2bn drop from the tip of the buyer EV tax credit score, and a $2.0bn hit from the tip of carbon tax credit. These proposals have been on the books now for per week or two, and haven’t moved the inventory all that a lot. With Trump and Musk now not on good phrases, it appears unlikely that Musk can persuade Republicans to amend the invoice.

The following chance is that the premium constructed into Tesla’s inventory is about extra than simply the automotive enterprise. Up till final week, it appeared that Musk’s corporations outdoors of Tesla had been getting a lift from his work within the federal authorities: X debt bought nicely, and SpaceX and Starlink received varied perks. Tesla buyers might need been anticipating one thing related for Tesla. Not now.

A remaining issue is partisanship. TD Cowen created a breakdown of Tesla’s US gross sales by every counties’ political leanings. Because the Trump-Musk partnership began, gross sales in purple counties have picked up and are a bigger share of the full, whereas gross sales have fallen in blue ones:

Itay Michaeli and his colleagues at TD Cowen observe that if all purple counties had been to achieve the identical degree of EV penetration as purple counties in Texas, which noticed a giant bump within the first quarter, there could be a 39 per cent bounce in EV gross sales this 12 months (not only for Tesla). However with Musk now on Trump’s unhealthy facet, Republican enthusiasm for EVs — Tesla’s EVs particularly — could wane.

There’s a vary of views about what may occur from right here. Whereas analyst estimates are largely ticking down, extra bullish assessments are on the market. Emmanuel Rosner at Wolfe Analysis argues that the hit from the price range invoice may very well be much less extreme than predicted by JPMorgan. He breaks it down as follows:

a) TSLA’s US tariff price is successfully zero, beneath opponents . . . within the ~$2000-$6000+ vary (creates a pricing umbrella); b) [Management] plans to launch an inexpensive line-up [likely leading to] wholesome margins at scale; and c) medium-term, with federal & state emission requirements easing, a number of automakers can be much less inclined to “push” EVs on to the market only for compliance functions [making a better EV pricing environment]

And who is aware of the place the connection between the 2 billionaires will wind up. Their love turned to hate faster than we imagined. However love and hate are at all times two sides of the identical coin. The bromance may very well be rekindled.

(Reiter)

The IPO market

American exceptionalism has been forged into doubt. We’re instructed that world buyers are turning in opposition to greenback belongings, or no less than hedging them far more fastidiously; that long-neglected inventory markets in the remainder of the world are having a second; that fiscal profligacy places US Treasuries’ standing because the pre-eminent world secure asset into query. And so forth. Unhedged is a bit sceptical about all this — whereas the speak is about revolution, what is going on in markets, checked out fastidiously, seems incremental.

Nowhere is the persistence of US exceptionalism extra obvious than within the IPO market. When corporations must faucet markets for fairness funding, it stays America or bust.

In simply the final week, the FT reported on two international corporations in search of to modify their main listings to the US: the massive Brazilian meat processor JBS, whose shareholders have already permitted the plan, and UK fintech Sensible. They aren’t the one ones contemplating the bounce. South Korean fintech firm Viva Republica and Chinese language electrical truck start-up Windrose are additionally choosing US IPOs.

Over the previous 10 years, international corporations have solely made up a modest share of US IPOs, as measured by deal worth. International share did go as excessive as 36 per cent in 2021, however that 12 months is anomalous as a result of huge Arm Holdings deal.

However wanting on the variety of offers, fairly than greenback quantity, the image is totally different — since 2023, abroad corporations have made up greater than 40 per cent of all of the IPO listings within the US. Thus far this 12 months, 60 non-US corporations have listed IPOs within the US, making up 43 per cent of the listings and 12 per cent of the full deal worth.

US corporations are staying personal longer, avoiding regulation and scrutiny, and profiting from the simple availability of personal funding. Volatility from Trump’s tariffs has additionally made it more durable for corporations to listing — lately, each Klarna and StubHub have needed to pause their debuts.

International corporations, nevertheless, seem undeterred by the coverage chaos within the US. And with good cause. Valuations within the US stay excessive, in relative phrases, regardless of weak point within the US fairness markets and robust efficiency from world markets. Europe’s Stoxx 600, for instance, trades at a median worth/earnings ratio of 17 versus 26 for the S&P 500. There’s much less restriction on government pay within the US, when it comes to each regulation and tradition. And the US gives excessive liquidity, a much bigger investor base that brings better passive funding flows, and the status of being related to the world’s largest exchanges. No different market is actually aggressive on these fronts.

Julian McManus at Janus Henderson thinks progress is the important thing:

Extra volatility, often all issues equal, will are inclined to imply a better fairness danger premium and a decrease valuation a number of; the US has managed to flee that rule till now. That is the exceptionalism half. And the explanation why it’s been in a position to be distinctive is as a result of the expansion charges that folks anticipate within the US are greater, and compensate buyers for that greater volatility. What stays to be seen is whether or not that continues to be the case.

American exceptionalism could degrade regularly over years. It has not disappeared in a single day.

(Kim)

One good learn

Let’s eat.

FT Unhedged podcast

Can’t get sufficient of Unhedged? Take heed to our new podcast, for a 15-minute dive into the most recent markets information and monetary headlines, twice per week. Atone for previous editions of the publication right here.

Really useful newsletters for you

Due Diligence — Prime tales from the world of company finance. Join right here

The Lex Publication — Lex, our funding column, breaks down the week’s key themes, with evaluation by award-winning writers. Join right here

{kind=link}