The Fed holds charges regular as anticipated… two dissenters for the primary time in a long time… Louis Navellier will not be pleased… GDP accelerates… India will get hits with a hefty tariff… a powerful ADP jobs report… final name for TradeSmith’s seasonality software

This afternoon, the Federal Reserve held the fed funds goal charge regular at 4.25% – 4.50% as was extensively anticipated.

Additionally anticipated – however extremely uncommon – have been the dissents from Fed governors Christopher Waller and Michelle Bowman. That is the primary time in additional than three a long time that two governors have dissented.

In Federal Reserve Chairman Jerome Powell’s reside press convention, he performed all his best hits: references to uncertainty… upcoming coverage selections being knowledge dependent… the necessity to steadiness the twin mandate… and so forth.

When requested if the agreed upon commerce offers have supplied sufficient knowledge for the Fed to raised forecast inflation, he hedged…

When requested a couple of lower in September, he demurred…

And when requested if tariffs have been in place lengthy sufficient to see their affect, he waffled and mentioned it’s “early days.”

Right here’s a short choice of what Powell was prepared to say:

- Waller and Bowman will lay out their reasoning for dissent within the coming days

- We’re not seeing weakening within the labor market, however there may be draw back threat

- Non-public sector job openings are down however so too are job seekers – no less than partially resulting from tighter immigration enforcement – so the labor market stays balanced

- The patron is in good condition however is now not spending quickly

- The consequences of tariffs on the buyer usually are not going to be zero

- The Fed will obtain its twin mandate of worth stability and most employment – Powell simply hopes they do it effectively

Again to the massive query – will September lastly convey the subsequent long-awaited charge lower?

The Fed Chair mentioned it’ll come all the way down to the “totality of the proof” and that “we now have made no selections about September.”

Whether or not the Fed cuts or not, legendary investor Louis Navellier believes they ought to.

Let’s go to his Accelerated Profits Weekly Situation from yesterday (I’ll get to his response to at present’s determination quickly):

There are a number of elements that ought to push a charge lower in September.

First, inflation has moderated.

Inflation has are available in beneath economists’ consensus estimate for 5 consecutive months. So, Fed Chair Jerome Powell’s fears of the inflation bogeyman have been unfounded.

Constructing on Louis’ level, even when we do see a flare-up in costs, why are we to imagine it will characterize an ongoing worth acceleration all through the financial system quite than a one-time worth bump on choose, tariff-affected items?

We dug into this challenge in our July 21 Digest. Put merely, worth will increase attributable to tariffs are totally different in nature and origin from these pushed by conventional inflation dynamics.

From that Digest:

A one-time tariff-based worth enhance doesn’t qualify because the sort of “inflation” that Powell & Co. are there to handle by coverage.

Tariff-based worth modifications don’t stem from an overheated financial system or extreme cash chasing restricted items. They occur as soon as – then patrons both change their conduct (shopping for a non-tariffed model) or they settle for the brand new, static larger worth for that particular good.

Both method, that new, tariff-impacted worth doesn’t all of the sudden endure from a brand new, larger inflation charge.

Theoretically, its inflation charge ought to be the identical because it was previous to that one-time worth bump.

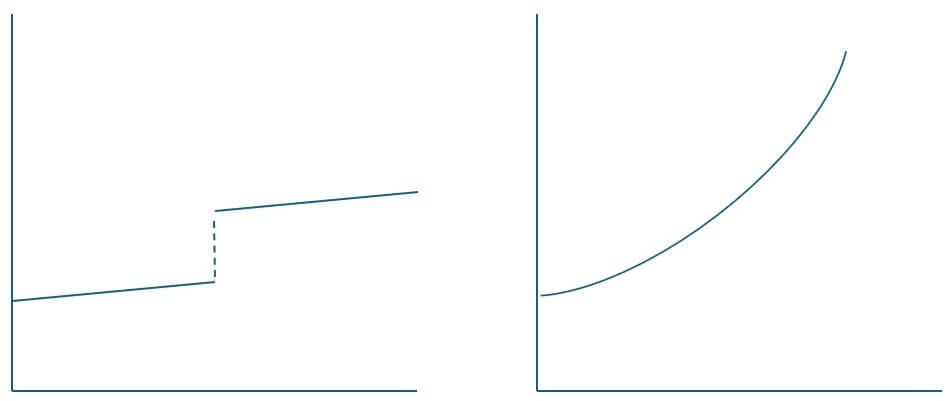

Beneath is the visible we supplied as an example.

One-time tariff-related worth will increase are on the left; the normal inflation dynamic is on the correct.

Now, because inflation has a huge psychological component, there is a risk: Consumers might see higher prices from tariffs, get confused about their origin, and then expect even higher prices to come, initiating the vicious inflation cycle.

This appears to be what Powell is concerned about – but that’s not happening today…

Consumer inflation expectations are falling

We have two recent pieces of data supporting this.

First, there’s the University of Michigan’s Consumer Sentiment Survey for July from two weeks ago, that showed tumbling inflation expectations.

From CNBC:

Consumers’ worst fears about tariff-induced inflation have receded…

The outlook at the one- and five-year horizons both tumbled, falling to their lowest levels since February, before President Donald Trump made his “liberation day” tariff announcement on April 2.

Second, there’s the Conference Board that reported more good news yesterday.

Here’s MarketWatch:

Consumer confidence rebounded modestly in July as Americans expected higher stock prices and easing inflation…

Their average 12-month inflation expectations eased slightly to 5.8% in July from a peak of 7% in April.

Yes, inflation expectations could flare back up, but the data tell us that – right now – they aren’t a problem.

Powell did address the difference between one‑time, pass-through inflation and ongoing inflation today

Here’s Powell from his press conference:

A reasonable base case is that the effects on inflation could be short‑lived, reflecting a one‑time shift in the price level.

But it is also possible that the inflationary effects could instead be more persistent, and that is a risk to be assessed and managed.

While that sounds balanced, Powell’s subsequent comment (and refusal to cut rates) shows what he really feels – we’re at greater risk of persistent inflation.

Back to Powell:

Our obligation is to keep longer-term inflation expectations well-anchored, and to prevent a one-time increase in the price level from becoming an ongoing inflation problem.

The second reason that Louis believes the Fed should cut in September

Let’s return to his Accelerated Profits Weekly Situation:

Second, there’s a mushy labor market…

Fed Governor Christopher Waller lately appeared on Bloomberg TV and laid out the case for why the Fed ought to lower key rates of interest to assist the labor market.

Particularly, Waller mentioned the U.S. financial system’s momentum has slowed considerably, and he expects it to “stay mushy” for the remainder of 2025.

We lined Waller’s speech right here within the Digest.

Let’s go to his remarks for extra element:

Whereas the labor market appears wonderful on the floor, as soon as we account for anticipated knowledge revisions, private-sector payroll development is close to stall pace, and different knowledge recommend that the draw back dangers to the labor market have elevated.

With inflation close to goal and the upside dangers to inflation restricted, we should always not wait till the labor market deteriorates earlier than we lower the coverage charge.

For Louis’ third cause, he factors towards falling international rates of interest:

The Financial institution of England and European Central Financial institution each have continued to chop key rates of interest this yr and have a pair extra charge cuts on the docket within the upcoming months…

As rates of interest proceed to break down, financial knowledge continues to melt and inflation stays tame, the Fed has no selection however to chop key rates of interest.

So, what was Louis’ total response to at present’s Fed determination?

Lower than enthused.

From Louis in at present’s Accelerated Profits Flash Alert:

The Fed Lives in a delusional world.

They’re saying that the financial system is unquestionably weakened…but it surely’s not time to chop charges but.

They’re arguing the labor division’s very sturdy…though plenty of that was seasonal changes.

So, I feel there’s an issue there.

Right here’s what’s actually occurring, people. The Fed lives in a delusional world.They’re not studying the information. Inflation has are available in beneath financial expectations for 5 straight months.

Now, Louis did say that the Fed might be chopping charges in September. He expects a vocal minority opposing it, however they’ll lower.

Again to Louis:

The Fed has to chop six instances.

So, they clearly have to begin chopping in September, lower once more in December and lower one other 4 instances subsequent yr. That’s what they should do.

The federal funds charge has to get to three%. I do know Trump requested for 1%, however they should get to three%.

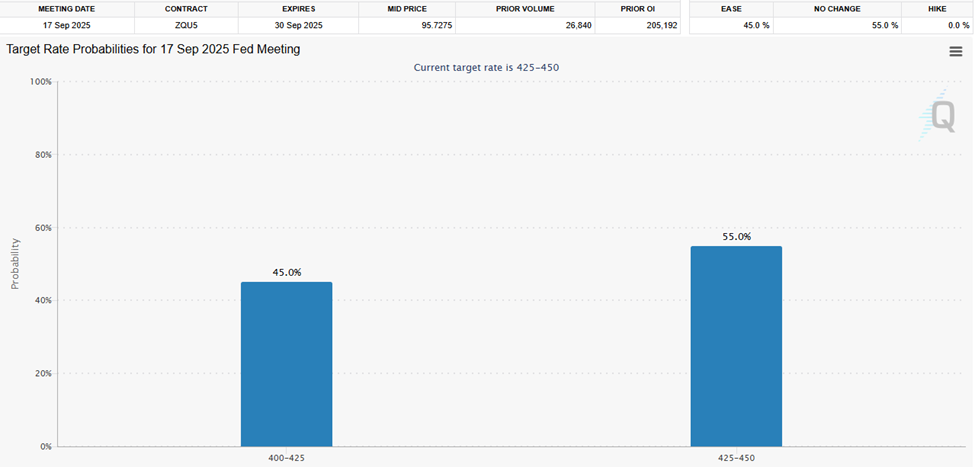

Futures merchants aren’t so certain – no less than for September…

As I write within the wake of at present’s announcement, the CME Group’s FedWatch Device reveals {that a} lower in September is principally a coinflip.

As you possibly can see beneath, whereas merchants put 45% odds on a quarter-point lower, 55% odds go to holding charges regular – once more.

Supply: CME Group

What’s most fascinating is that just yesterday, those 55% odds clocked in at only 35.4% odds.

Clearly traders interpreted Powell as hawkish today.

So, plenty of big questions going forward. We’ll keep you updated as we hear more from Louis, the dissenting Fed governors, and Powell.

A tour through three additional big headlines today

The FOMC meeting wasn’t the only news of the day. We also got an updated GDP print, details of the new tariff on India, and the ADP jobs report.

Beginning with the economy, the Commerce Department’s advance estimate showed that U.S. real GDP grew at an annualized 3.0% pace last quarter. That’s a strong rebound from the ‑0.5% contraction in Q1 2025.

However, this upside surprise was driven largely by a sharp drop in imports as businesses front‑loaded inventories ahead of tariff hikes.

Zeroing in on consumers, while they’re not rolling over, neither are they out there spending up a storm.

Here’s Mark Zandi, chief economist at Moody’s Analytics:

You abstract from all of the tariff-related ups, downs and arounds, and the underlying story is that the economy is struggling. The economy has significantly throttled back this year…

Consumer spending was very strong coming out of the pandemic. But since December, it’s flatlined.

The American consumer may not be pulling back, but they are certainly sitting on their hands.

Let’s take this as a mixed win. GDP is strong but the most important driver – consumer spending – has fragile momentum.

Moving on to tariffs, President Trump announced via Truth Social that starting Friday (the August 1 deadline), a 25% tariff will be imposed on Indian exports.

As to why, Trump pointed toward trade imbalances, India’s high non‑monetary trade barriers, and its continued purchase of Russian weapons and energy.

Now, India isn’t a huge trading partner for the U.S., but the relationship is strategically important. So, the tariff seems to be more about geographic/political leverage given India’s trading relationship with Russia.

We’ll see whether this move ultimately strengthens relations with the U.S. or pushes India closer to the BRICS nations.

Finally, ADP reported that private-sector employers added 104,000 jobs in July. This was a sharp reversal from a revised 23,000-job loss in June and well above the forecast of about 75,000 jobs. It was also the largest monthly gain since March.

From ADP’s Chief Economist Dr. Nela Richardson:

Our hiring and pay data are broadly indicative of a healthy economy. Employers have grown more optimistic that consumers, the backbone of the economy, will remain resilient.

While we’re encouraged, what really matters is the official U.S. employment report on Friday. Forecasters are looking for growth of 100,000 jobs.

We’ll report back.

Finally, it’s last call to check out one of the most powerful quant-based trading tools on the market today

Last week, Keith Kaplan, CEO of our corporate partner, TradeSmith, and Louis hosted an online briefing to profile TradeSmith’s seasonality tool.

Here’s Keith with some background:

For the past three years, we’ve been developing software that can spot hidden seasonality patterns in the stock market.

The basic idea is that certain price trends repeat year after year, regardless – not unlike the nature’s seasons.

Stocks don’t have summers and winters exactly. But we’ve been able to identify consistent, repeating cycles in stocks, currencies, and even commodities like oil and soybeans…

These patterns are hard for humans to see. But our software reviews decades of market history for thousands of stocks, indexes, and commodities—to pinpoint the moments when prices tend to turn, down to the calendar day.

To give you an illustration of how it works, let’s look at the S&P.

The seasonality tool has flagged a major regime change – beginning now.

As you can see in the chart below, we’ve just wrapped up one of the tool’s green seasonal windows when the index has historically risen, year after year.

But I’ve circled what comes next…

Back to Keith for the details:

We have gotten a top around July 28. Then the market has stumbled before bottoming out in October.

Over the past 15 years, the S&P 500 has had an average return of -1.6%, falling as much as 15% during this window.

This doesn’t mean you need to get out of the market…

But it does suggest three responses:

- Be ready for pullbacks and don’t let them shake you out of your high-conviction, long-term positions

- Limit your bullish short-term trades to only those stocks that, historically, have shown they can climb during this historically weak season

- Get cash ready to plow into to your high-conviction holds when they near their seasonal lows in the upcoming months

The seasonality tool can be a huge help with all three action steps. To see how with Keith and Louis, click here to catch the free replay of their broadcast from last week. I’ll add that that is final name – the replay goes down tonight.

We’ll hold you up to date on all these tales right here within the Digest.

Have a great night,

Jeff Remsburg

{kind=link}