For those who’ve ever heard older people speak about the best way the housing market was ‘again of their day,’ it most likely sounded extra like fiction than reality. I’ll always remember how bewildered I felt when my grandmother instructed me her first home value $11,000…

At the moment – within the early Nineteen Fifties – the common dwelling worth was round $8,000, whereas common family earnings was about $4,000 per yr. In different phrases, the price-to-income ratio again then was about 2:1 – far and away from right now’s actuality, estimated between four- and 5X earnings.

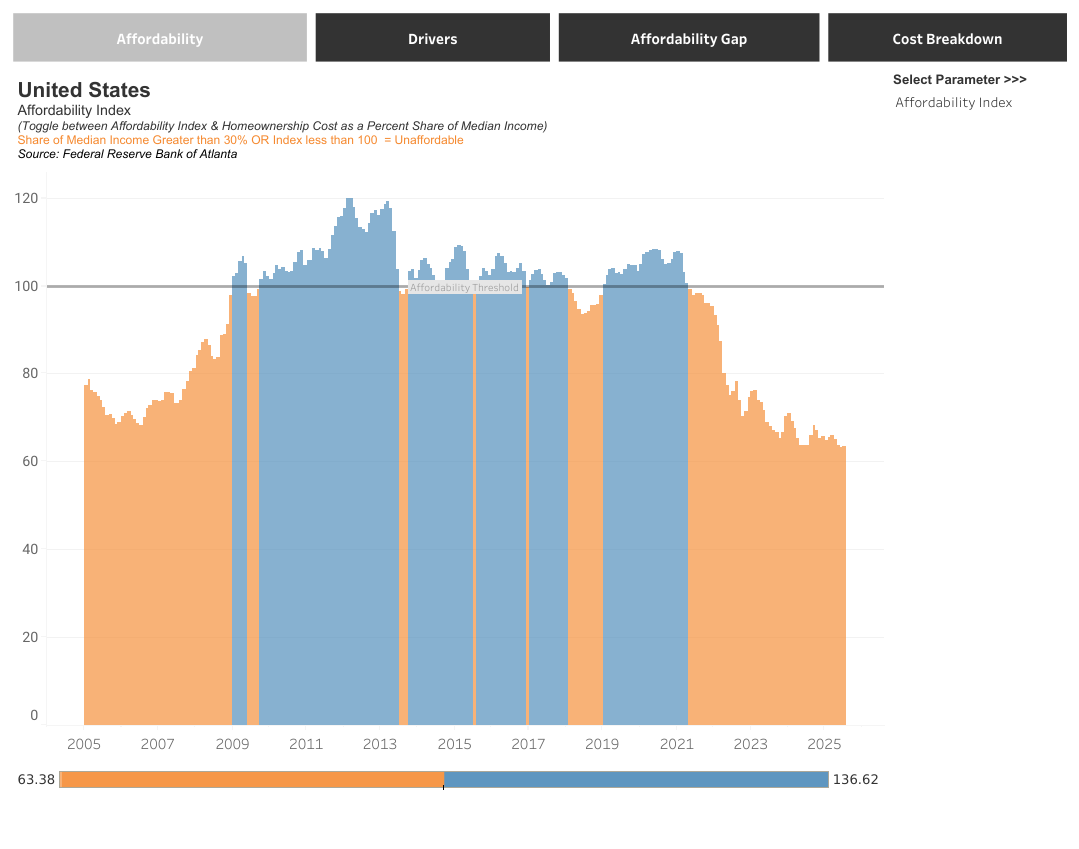

By virtually each measure, affordability is at all-time lows…

Sadly, provide is caught close to document lows as effectively. As of July 2025, America’s housing scarcity has grown to an all-time excessive of 4.7 million models, in accordance with research from Zillow.

Youthful individuals can’t afford to purchase. Older householders aren’t promoting. New building hasn’t saved up with demand. The end result? The worst housing disaster in fashionable U.S. historical past.

However the White Home could also be gearing as much as do one thing about it.

Treasury Secretary Scott Bessent lately hinted that the administration might declare a Nationwide Housing Emergency this fall. He didn’t share particulars, however make no mistake: Washington has loads of levers it might pull to reset this market.

We’re speaking tariff and material-cost reduction, incentives and grants for first-time consumers, down-payment help, streamlined allowing, modifications in housing finance, even the usage of federal land for brand spanking new improvement.

If that occurs, the market will thaw; and housing shares ought to fly…

Which means this can be a prime time to begin accumulating housing-related names.

How the Housing Disaster Reached a Breaking Level

To grasp why a coverage shock might matter a lot, you must perceive simply how damaged issues are.

Over the previous 4 a long time, the U.S. housing market was outlined by one structural tailwind: falling mortgage charges. From the early Nineteen Eighties till the early 2020s, 30-year mortgage charges trended down, enabling consumers to afford increased dwelling costs whereas protecting month-to-month funds manageable.

That every one modified in 2022.

Between early 2022 and late 2023, mortgage charges spiked from 3% to eight%. That’s a 500-basis-point transfer – the steepest enhance on document, with knowledge going again to 1990. And charges haven’t actually come down since. The typical 30-year mortgage has hovered round 7% for 2 years now.

The impression on demand has been devastating. Zillow knowledge exhibits that U.S. households at the moment are spending a median of greater than 35% of their yearly earnings on mortgage funds for a brand new dwelling, in comparison with lower than 25% only a few years in the past.

Something above 30% is taken into account “unaffordable.” Bloomberg estimates that you just want almost $120,000 in annual earnings to afford the common dwelling right now. However the median U.S. family earnings? About $80,000. That math merely doesn’t work.

In fact, excessive charges didn’t simply destroy demand. They froze provide, too.

Anybody who purchased a house within the final 25 years virtually actually locked in a mortgage price effectively beneath right now’s market. Unsurprisingly, informal sellers have vanished. Why would you commerce a 3% mortgage for a 7% one? The one individuals placing properties available on the market are those that have to maneuver. On high of that, elevated borrowing prices have made constructing new properties costlier, choking off contemporary provide.

So, right here we’re: low demand, low provide, sticky-high costs, and affordability within the gutter.

The Fed Can’t Repair Housing Alone

Now, price cuts might assist, and the Federal Reserve has began down that highway. However let’s be reasonable: this market is simply too damaged for financial coverage alone to repair. It would take a coverage sledgehammer.

That’s the place the White Home is available in.

If the administration does transfer ahead with a Nationwide Housing Emergency, it has a number of levers it might pull, a lot of which might have quick, tangible impacts:

- Tariff and materials value reduction. Decreasing tariffs or granting exemptions on imported lumber, metal, or different key constructing supplies might instantly decrease building prices.

- First-time purchaser assist. Grants, down-payment help, or expanded Federal Housing Administration (FHA) advantages would straight ease affordability challenges.

- Regulatory streamlining. Federal steering might push localities to speed up allowing timelines, particularly on multifamily and inexpensive housing initiatives.

- Mortgage finance tweaks. Businesses just like the Federal Housing Finance Company (FHFA) and Division of Housing and City Improvement (HUD) might reduce charges or loosen restrictions, whereas Fannie Mae and Freddie Mac may very well be nudged towards extra versatile underwriting or focused inexpensive housing initiatives.

- Use of federal land. Giant swaths of federally owned land may very well be opened to housing improvement, significantly in areas the place zoning and native politics have created bottlenecks.

Individually, none of those measures would repair the housing market. However mixed, they might meaningfully increase each provide and demand inside a yr. And that’s the type of synchronized intervention that might set off a housing growth not like something we’ve seen for the reason that post-financial-crisis rebound almost 20 years in the past.

The Inventory Market Angle: Housing Shares That May Soar

If the White Home pulls this set off, housing-related shares ought to rip.

The plain commerce is in homebuilders.

Lennar (LEN), PulteGroup (PHM), DR Horton (DHI), KB Dwelling (KBH), NVR (NVR), Toll Brothers (TOL), Meritage Houses (MTH), Inexperienced Brick Companions (GRBK) – these are the blue chips of America’s housing building business. They’ll profit straight from any increase in demand, decrease materials prices, or sooner allowing timelines. Their order books will swell, their margins will broaden, and their earnings will leap.

However right here’s the place I’d go a step additional: the true upside lies in housing tech.

- Zillow (Z): The closest factor we have now to a digital super-app for housing. If extra consumers flood the market, Zillow turns into the go-to platform, particularly for millennials and Gen Z.

- Opendoor (OPEN): The iBuying mannequin thrives in higher-volume markets. If Washington can thaw out provide, Opendoor’s algorithm-driven immediate affords will look more and more enticing to sellers.

- Compass (COMP): A tech-first brokerage that might win market share as brokers flock to platforms providing higher digital instruments.

- Rocket Mortgage (RKT): A policy-driven housing growth paired with falling mortgage charges might unleash a large refi wave. And Rocket dominates that area; maybe the most important winner of all of them.

These are structural disruptors poised to realize share as housing transactions migrate on-line. And a Nationwide Housing Emergency may very well be the catalyst that accelerates that shift.

Why Traders Have to Place for Housing Now

Housing affordability is changing into a generational concern, and it’s climbing the coverage agenda.

The administration is in search of wins heading into 2026. And in contrast to many avenues, housing intervention has the potential to ship seen, near-term reduction to thousands and thousands of households.

And since markets are forward-looking, if the White Home even hints at a concrete emergency bundle, housing shares might hole increased in a single day.

Ready till the small print are out will imply lacking a lot of the transfer. That’s why now could be the second to begin constructing publicity. Whether or not via the builders or the tech disruptors – or each – traders who place forward of a Nationwide Housing Emergency declaration may very well be one of many strongest tailwinds of the following 12 months.

And we expect it might occur any day now. In that case, the mixed impression of decrease materials prices, extra federal land, simpler mortgages, and assist for first-time consumers might set off a growth not like something we’ve seen for the reason that 2008 monetary disaster.

The builders will profit. However the true uneven upside lies within the housing tech stack – names like Zillow, Opendoor, Compass, and Rocket Mortgage.

We face the worst affordability crunch in fashionable historical past. That’s the issue. The chance? When the coverage hammer falls, the rebound might mint fortunes.

Most traders received’t know the place to look… However Eric Fry’s Apogee system does.

It’s already recognized 5 shares getting into what he calls the “10X Zone.” And Eric is revealing every ticker right now – before the crowd catches on.

However if you wish to know extra, time is of the essence: this provide closes at midnight.

{kind=link}