Jobs information exhibits a cooling financial system… unemployment ramps larger than anticipated… the “shadow chair” is coming – however who will or not it’s?… completely different charge minimize paths, however the identical vacation spot?

Right this moment’s much-anticipated employment report lastly arrived, and it delivered a story of two months.

Following the 43-day federal authorities shutdown, which delayed information, the Bureau of Labor Statistics reported a pointy lack of 105,000 jobs in October, adopted by a modest achieve of 64,000 in November.

That November achieve did beat expectations, however it hardly indicators sturdy demand. Roughly 70% of all job creation got here from the healthcare sector, that means that development was removed from broad-based.

A very powerful determine this morning wasn’t payrolls in any respect – it was the unemployment charge, which climbed to 4.6% in November, its highest stage in additional than 4 years.

That issues as a result of, simply final week, the Fed’s up to date dot plot confirmed policymakers anticipating unemployment to peak at 4.5% this 12 months earlier than starting to ease decrease. So, we’re already above that projection.

Now, to be honest, the BLS – and Powell himself – warned that the federal government shutdown may distort the information, probably pushing unemployment larger within the quick time period. So, this 4.6% studying must be taken with a grain of salt.

Nonetheless, the broader image wasn’t encouraging. Right here’s CNBC:

A extra encompassing measure that features discouraged employees and people holding part-time jobs for financial causes swelled to eight.7%, its peak going again to August 2021.

So, what are we to make of this as buyers?

Effectively, the labor isn’t collapsing, however it’s clearly cooling. That’s not nice information for sustained shopper spending, which accounts for roughly 70% of the U.S. financial system.

Then again, the rising unemployment charge may nudge policymakers to ease monetary circumstances. However this isn’t a foregone conclusion for a number of causes:

- The 64,000-job achieve got here in above expectations

- Right this moment’s information possible wasn’t weak sufficient to disrupt Powell’s “wait-and-see” stance from final week

- There’s nonetheless the inflation a part of the equation (we get the brand new CPI report this week).

Total, the Fed isn’t reacting to at least one or two jobs reviews. It’s watching a wider mixture of inflation and development information.

In the meantime, one other drama is unfolding – one that might find yourself having way more affect over charge coverage than any single jobs report… and even a number of months’ price of them.

The Fed’s public message vs. its personal actuality

Formally, the Fed stays affected person, data-dependent, and noncommittal.

As Powell put it final Wednesday:

We’re well-positioned to attend and see how the financial system evolves from right here.

Wall Road heard that and shortly pulled again expectations for near-term cuts. And this morning’s information hasn’t modified that.

As I write on Tuesday, the CME Group’s FedWatch Instrument places the chance of a minimize in March as a toss-up. April is the primary month when merchants assign majority odds to the subsequent quarter-point minimize.

Nevertheless, in accordance with our hypergrowth knowledgeable, Luke Lango of Innovation Investor, merchants anticipating a sleepy, inactive Fed over the subsequent few months have it improper.

Luke has written that the subsequent handful of months will deliver the rise of a “shadow chair.” Somebody with out the gavel but – however with rising affect:

FOMC members will know who’s coming. They’ll know the way that particular person thinks about inflation, unemployment, and asset costs.

Simply as importantly, Luke says these Fed members will perceive the political backdrop:

Trump needs a robust financial system and robust markets heading into the 2026 midterms, not some tutorial experiment in tight cash.

Put all of it collectively, and Luke expects a transition interval the place the Fed is publicly cautious, whereas privately getting ready for slower development – and more and more factoring within the preferences of a chair-elect who could also be extra inclined to ease than present forecasts counsel.

Right here’s what this implies for charges:

The chances of extra cuts by spring are in all probability larger than what the market is at the moment pricing.

So, who is that this shadow chair?

Does a brand new wrinkle complicate Luke’s forecast?

Till lately, Luke has been clear about his expectation: Kevin Hassett is the possible candidate to be the subsequent Fed chair.

Hassett is a former Trump financial adviser with a protracted file of emphasizing development dangers, market stability, and the hazard of overtightening.

He suits cleanly into Luke’s “shadow chair” framework — a chair-elect who would quietly give the Fed’s dovish wing cowl to ease coverage because the financial system cools.

In that state of affairs, the logic is easy: a growth-friendly chair… extra consolation reducing charges… simpler monetary circumstances into 2026… shares applaud.

Now, whereas Hassett stays a number one contender for the position, over the previous a number of days, a brand new twist has emerged – one which doesn’t overturn Luke’s thesis, however does add nuance to the way it might play out.

Enter Kevin Warsh

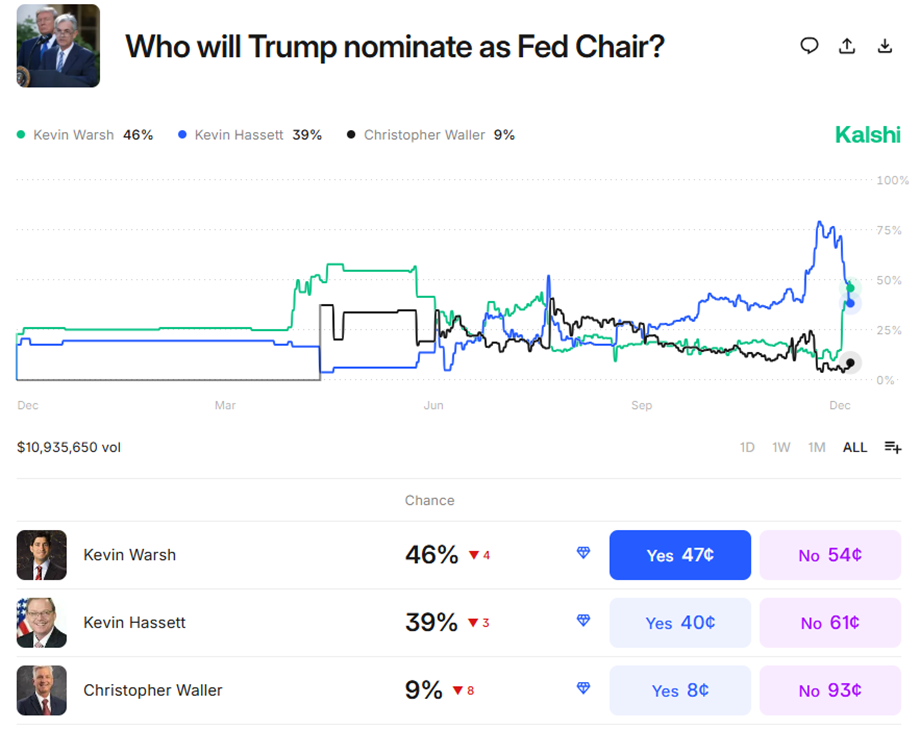

Former Fed Governor Kevin Warsh has now emerged as a critical – and presumably main – contender.

Earlier this morning, the predictive markets platform Kalshi put Warsh within the prime spot, assigning him roughly 46% odds of getting the nomination, in contrast with 39% for Hassett.

Supply: Kalshi

Now, at first look, this might sound complicated.

Warsh is extensively considered as extra hawkish than Hassett – extra targeted on inflation credibility, extra important of QE, and extra skeptical of the Fed’s position in inflating asset costs.

So why would President Trump – who needs meaningfully decrease charges – lean on this course?

Most likely as a result of Trump isn’t viewing this concern purely as “who will minimize probably the most?” He’s additionally desirous about the politics of the choice, and asking himself, “Who can minimize with out triggering a backlash?”

And that is the place Warsh brings one thing Hassett doesn’t…

What Warsh would give Trump

To the markets – particularly bond markets – Warsh appears like somebody who won’t ease recklessly or for political causes. He speaks the language of central financial institution independence.

This credibility issues.

A chair perceived as too dovish from day one dangers pushing long-term yields larger, strengthening the greenback, and undermining the very easing that Trump needs.

Plus, virtually talking, even when Trump needs Hassett extra, he may need a better time getting Warsh by means of affirmation politics.

A former Fed governor with institution bona fides is usually less complicated to shepherd by means of the method than a sitting or latest White Home insider – and also you’ve in all probability observed how a lot of the press protection frames this as Warsh the “institutional” possibility versus Hassett the “Trump loyalist.”

So, right here’s what Trump is perhaps pondering…

Hassett makes me appear to be I’m establishing a puppet chair.

Warsh will sound harder on inflation at first, however that doesn’t imply he gained’t minimize later with much less resistance.

This morning, Hassett tried to push again on this, saying:

The Federal Reserve’s independence is absolutely, actually essential, and the voices of the opposite individuals on the [Federal Open Market Committee], they’re essential, too…

The concept that somebody isn’t certified for the job as a result of they’re an in depth buddy who’s labored nicely with the president is one thing that I feel the President rejects.

Shockingly, it seems this may need labored – at the least in accordance with Kalshi. As we’re going to press, Hassett is again within the lead…

Now, given how shortly these odds transfer, let’s proceed with our concentrate on Warsh because the potential new Fed chair.

If he’s extra hawkish, why ought to we consider he’ll minimize charges in any respect?

Why the rate-cutting narrative remains to be in play

The case for Warsh reducing later rests on how hawkish chairs have traditionally behaved, not on Warsh reworking right into a dove or succumbing to strain from Trump.

First, as simply famous, Warsh’s credibility issues to the markets. It buys flexibility.

A chair who establishes inflation self-discipline early can ease later with out spooking Wall Road. Bond buyers have a tendency to withstand cuts from somebody they don’t belief – however as soon as belief is established, resistance fades when/if development slows.

In the meantime, Warsh isn’t blind. This morning’s information exhibits that the financial system isn’t precisely firing on all cylinders. So, if/when the information deteriorates additional, he’s more likely to reply – which brings us to the subsequent level…

Warsh is mostly data-driven, not a hardline hawk.

Whereas he’s been important of QE and extra liquidity, he’s by no means argued that coverage ought to ignore labor-market weak point. So, if unemployment continues to rise and development slows, his stance would possible assist charge cuts – simply later and with clearer justification.

Lastly, politics nonetheless applies.

No Fed chair – hawkish or not – needs to preside over a deep slowdown heading into an election cycle if the information clearly argues for reduction.

So, the principle distinction between these two prime contenders is that Hassett would possible pull cuts ahead, whereas Warsh would possible delay them – then face much less resistance when the time comes.

That’s the trade-off Trump might be weighing.

None of this contradicts Luke’s core level. The Fed remains to be transitioning away from “crush inflation in any respect prices,” and a management change nonetheless weakens Powell’s grip.

So, whether or not it’s Hassett or Warsh, the concept the Fed merely goes dormant for months – and delivers solely a single charge minimize in 2026 – is probably going an oversimplification.

Backside line…

Right this moment’s unemployment report confirms what we knew – the labor market is cooling however not at a panic-inducing charge. By itself, that provides the Fed cowl to remain affected person and stick to its wait-and-see stance.

However job information isn’t the one factor that may decide the place charges go subsequent. Clearly, who leads the Fed issues too.

At first look, the distinction between Hassett and Warsh appears significant. However if you dig in, the excellence could also be much less about the place charges are headed and extra about how and after they get there.

We’ll give Luke the underside line:

[Trump’s] “shadow chair” will start shaping coverage lengthy earlier than the official transition.

Charges are nonetheless headed meaningfully decrease in 2026.

The trail might wobble, however the vacation spot hasn’t modified.

Keep constructive, keep opportunistic, and maintain shopping for nice AI names on weak point.

Have an excellent night,

Jeff Remsburg

{kind=link}