The TL;DR abstract:

-

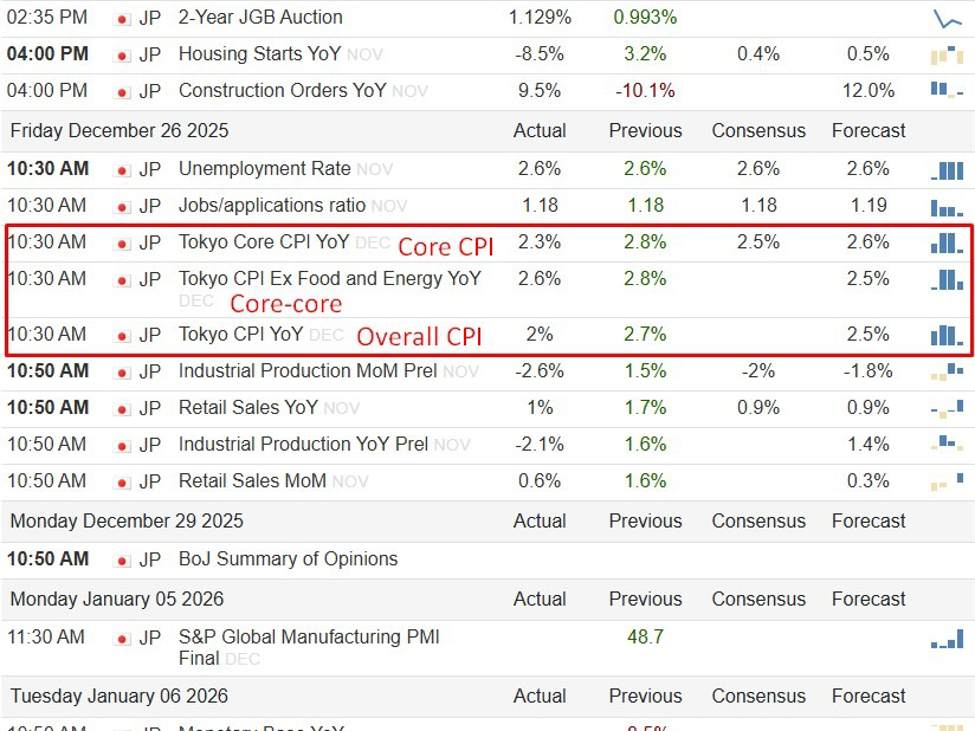

Tokyo core CPI slowed to 2.3% y/y in Dec (vs. prev 2.8%, exp 2.5%), pushed by decrease vitality and utility prices.

-

Core-core CPI eased to 2.6% y/y (prev 2.8%), however stays above the BOJ’s 2% goal, signalling persistent demand-side stress.

-

Headline CPI cooled to 2.0% y/y (prev 2.7%), marking the primary clear deceleration since August.

-

Information softens urgency, not course, of BOJ coverage; inflation stays in keeping with gradual additional tightening after final week’s hike to 0.75%.

-

Market read-through: modest yen softness close to time period, JGB front-end consolidation, Nikkei supported by diminished fast tightening threat.

The screenshot above is through TradingEconomics.

—

Tokyo inflation cooled greater than anticipated in December, however remained comfortably above the Financial institution of Japan’s 2% goal, preserving the coverage normalisation story intact whilst near-term urgency eased.

Core client costs within the capital, excluding recent meals, rose 2.3% y/y, slowing from 2.8% in November and undershooting market expectations of two.5%. The deceleration was pushed largely by decrease utility and vitality prices, alongside a moderation in meals value features.

A intently watched “core-core” measure that strips out each recent meals and vitality additionally softened, easing to 2.6% y/y from 2.8% beforehand, whereas headline CPI slowed to 2.0% from 2.7%. Collectively, the figures marked the primary clear easing in Tokyo inflation momentum since August.

Regardless of the slowdown, all three gauges stay at or above the BOJ’s inflation goal, reinforcing the view that underlying value pressures have grow to be entrenched. Tokyo CPI is extensively considered a number one indicator for nationwide traits, suggesting inflation is cooling regularly moderately than collapsing.

The info follows final week’s Financial institution of Japan determination to boost its coverage price to 0.75%, the best degree in roughly three a long time. Governor Kazuo Ueda has careworn that additional tightening will observe if wages and costs evolve in step with the central financial institution’s outlook, whereas intentionally avoiding steering on tempo or terminal ranges.

Markets now see the December information as in keeping with the BOJ’s baseline state of affairs: inflation easing as vitality results fade, however remaining sufficiently agency to justify extra price hikes over time. Analysts proceed to anticipate a gradual climbing cycle, with charges rising roughly each six months and a terminal degree close to 1.25%, assuming wage progress stays strong.

BOJ coverage implications

The softer-than-expected core print barely reduces stress for an imminent follow-up hike however does little to derail the broader tightening trajectory. With core inflation nonetheless above goal and wage dynamics supportive, the BOJ is prone to proceed cautiously. A pause appears seemingly on the subsequent assembly, on January 22–23, 2026.

Market influence: yen, JGBs, Nikkei:

-

Yen: The draw back CPI shock could cap near-term yen features, particularly if US yields stay elevated, however persistent above-target inflation limits scope for sustained depreciation.

-

JGBs: Entrance-end yields could consolidate after the latest sell-off, although the medium-term bias stays towards greater yields as coverage normalisation continues.

-

Nikkei: Equities could welcome diminished near-term tightening stress, notably rate-sensitive sectors, whereas exporters stay delicate to yen swings.

{kind=link}