Abstract:

-

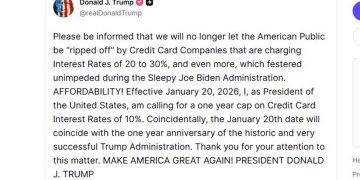

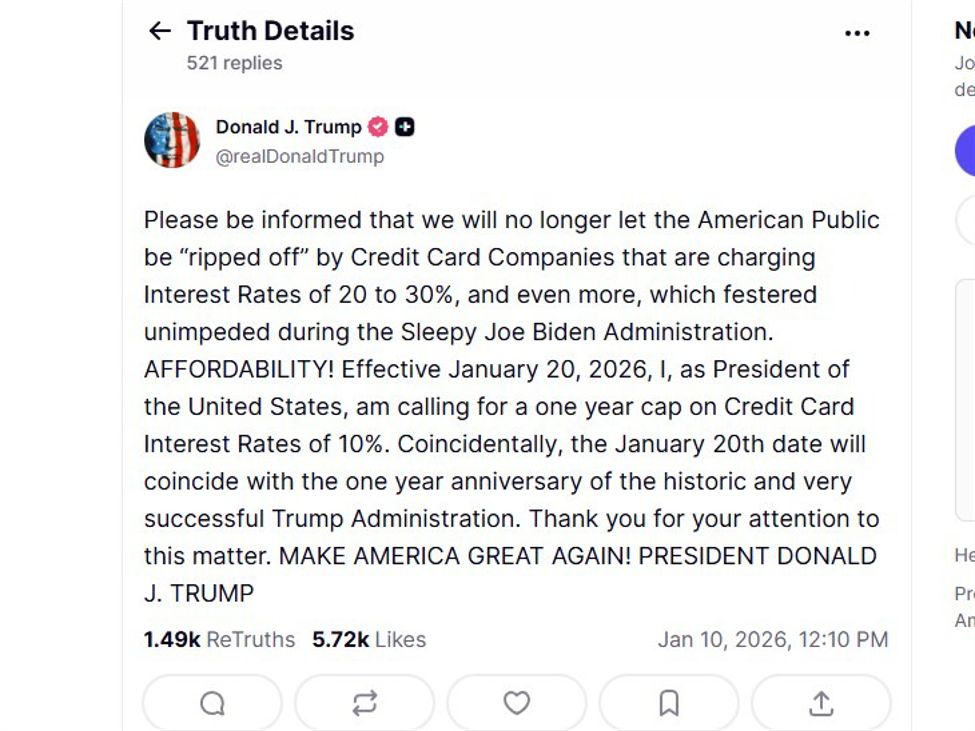

Trump requires 10% credit-card APR cap for one 12 months, efficient Jan 20, 2026.

-

No enforcement element: unclear if voluntary or government-mandated.

-

A part of a populist “affordability” burst this week (incl. MBS shopping for concept and ban on institutional residence consumers).

-

Huge hole to present pricing: Fed knowledge reveals 22.30% (Nov 2025) on the important thing credit-card charge collection.

-

With out laws / clear authority, this seems to be like headline politics first, coverage mechanics later.

President Donald Trump has referred to as for a one-year cap of 10% on US credit-card rates of interest, saying shoppers are being “ripped off” and framing the transfer as an “affordability” push. The proposal would begin January 20, 2026, the primary anniversary of his return to the White Home, however Trump offered no element on the mechanism, leaving open whether or not he expects voluntary compliance from issuers or is signalling some type of authorities enforcement.

The shortage of element issues, as a result of credit-card pricing is just not one thing a president can merely “announce” into existence. In follow, a tough cap would usually require Congressional laws and/or actions by means of the US regulatory framework. But the primary federal watchdog for card practices, the Shopper Monetary Safety Bureau (CFPB), has been a long-running goal of conservatives, and the Trump administration has pursued steps that would scale back or constrain its attain.

What Trump is doing, clearly, is leaning right into a string of populist, social-media-first affordability declarations this week, excessive on punchy intent, low on executable element. Within the days prior he posted about ordering “his representatives” to purchase mortgage bonds to push borrowing prices decrease, and about banning institutional buyers from shopping for single-family properties. Collectively, the sequence reads as an try and reclaim the cost-of-living narrative with easy targets (banks, Wall Road, establishments) and headline-friendly numbers (10%). This all, in fact, in an election 12 months (mid-terms) with Trump’s recognition persevering with to make new lows and due to this fact threatening the Republican majorities in Congress. I posted earlier within the week that I count on populist bulletins and an eventual hit to the US greenback (not but although, the greenback greater on Friday: investingLive Americas market information wrap: Nonfarm payrolls a contact comfortable, no tariff resolution)

On the numbers, the coverage could be a dramatic lower versus prevailing charges: the Federal Reserve’s collection for business financial institution credit-card curiosity (accounts assessed curiosity) reveals ~22.30% in late 2025. That hole underscores why markets and issuers will concentrate on “how” somewhat than “what”, and why, and not using a clear legislative pathway, the announcement seems to be extra like political signalling than an instantly actionable coverage shift.

Congressional curiosity in caps is actual and notably bipartisan, previous proposals have sought a ten% ceiling, however they haven’t change into legislation. Till a invoice advances (or a reputable regulatory/administrative route is spelled out), the more than likely near-term influence is messaging and volatility in associated headlines, somewhat than an immediate repricing of shopper credit score.

{kind=link}