Money App, the peer-to-peer fintech app owned by Jack Dorsey’s Block, has launched a brand new “pay-over-time” deferred cost function that enables eligible customers to pay for his or her on a regular basis transfers over an prolonged time period.

Firms have more and more supplied deferred funds for comparatively mundane and on a regular basis purchases. A few yr in the past, DoorDash partnered with Klarna — permitting customers to “micro-finance” their meals orders (the partnership notably impressed a flurry of on-line jokes about “burrito debt” and late capitalism). Money App’s new function clearly builds on this development — increasing versatile financing into the P2P cost realm.

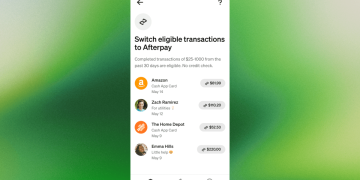

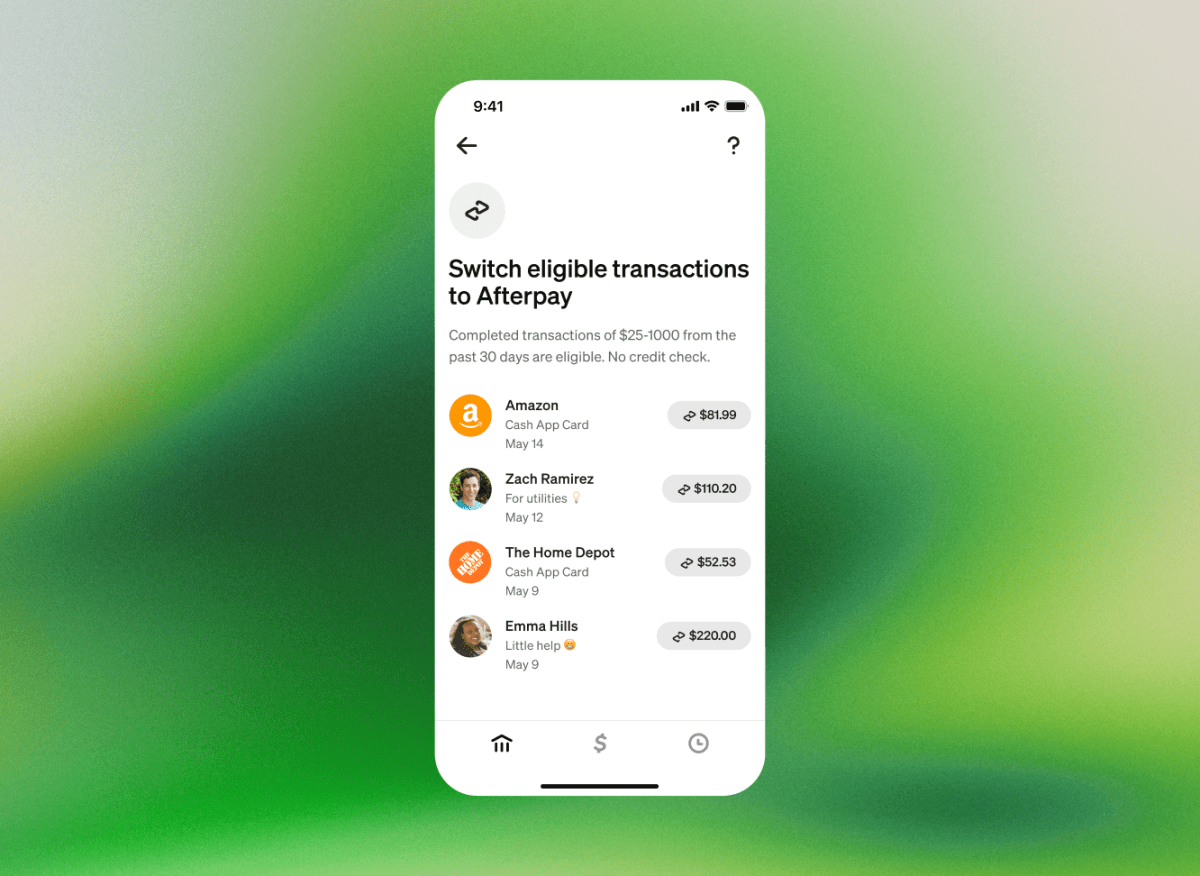

To reap the benefits of the brand new function, customers pay a 7.5% price — that means that, in case you borrow $100 from Money App, you’re going to finish up paying the corporate again $107.50. Transfers of $25 or extra are eligible, the corporate says, and repayments might be made in weekly increments over a interval of as much as six weeks or as a single cost on the due date.

There are additionally mortgage limits to the brand new system, however they’re dynamic — that means that they are going to be completely different for various customers. “The particular quantity accessible for conversion relies on the unique transaction quantity and particular person buyer evaluation,” a spokesperson stated. “We consider every transaction for eligibility primarily based on our accountable lending standards somewhat than setting conventional credit score limits,” they added.

In an interview, Block’s Govt Officer and Head of Enterprise, Owen Jennings, framed the brand new function as a method so as to add worth to Money App’s prospects through “money movement administration.” Jennings famous that many People have completely different sorts of jobs immediately — lots of which pay with much less consistency than these supplied in prior a long time. Money App’s new function is designed so as to add monetary flexibility to that scenario, Jennings stated.

“We’re seeing extra of us — significantly youthful of us — who’re solo-preneurs, entrepreneurs … [and] gig staff. They’ve facet hustles, they’re working a number of jobs, [and] so that they have variable revenue streams,” Jennings stated. “It’s very completely different than in case you return like 40 or 50 years in the past — I believe the common revenue earner within the U.S. [back then] was mainly getting, like a gentle W2 revenue each two weeks.”

“Purchase now, pay later” companies have skyrocketed in reputation over the previous a number of years whereas additionally spurring vital criticism and concern. Some critics keep that such companies are designed to entice shoppers in cycles of debt, whereas others have recommended that People needing to finance primary home items is an indication of broader financial disaster. Firms that present these companies have additionally discovered themselves in authorized scorching water. Simply this week, Klarna was sued in a class-action lawsuit alleging it had engaged in “predatory” practices, Bloomberg experiences.

Techcrunch occasion

San Francisco, CA

|

October 13-15, 2026

Jennings stated Money App’s new function has robust built-in protections which are designed to steer customers away from monetary bother, like getting caught in what he known as “debt spirals.” “The way in which all of our lending merchandise are created is non-revolving,” he added. “In case you don’t pay again a mortgage, then you’ll be able to’t take out one other mortgage.”

The service additionally builds off of different monetary flexibility companies that Money App already provides, Jennings stated. In prior years, the app debuted Borrow, which, considerably like a standard financial institution, permits customers to take out a small mortgage from the app after which pay it again over a interval of 4 to 6 weeks.

One other providing is Afterpay for Money App Card (its debit program), which permits customers to defer funds for transactions made with the cardboard.

{kind=link}