Markets erupt increased… is that this rebound actual or a brief?… diagnosing why shares are falling… the dance between sentiment and earnings… don’t miss Louis Navellier’s 50X small-cap concept

As I write Friday, shares are ripping increased.

Is that this the start of a sustained, bullish rebound? Or bullish idiot’s gold earlier than the following leg decrease?

To assist reply this, let’s diagnose the issue.

The market presently has a “sentiment” drawback.

The excellent news is that – no less than for the second – it’s not an “earnings” drawback as effectively. And that ought to restrict how a lot draw back stays in entrance of us, if there’s any in any respect.

Let’s break this down.

There are two key variables that affect the value of every inventory you personal

- The earnings of your underlying corporations

- The a number of that traders are prepared to pay for these earnings – which we are able to consider as “investor sentiment”

Within the short-run, investor sentiment is definitely the best affect on inventory costs.

On any given day, gleeful or despondent traders can drive shares to unfathomable heights or depths primarily based on greed and worry.

However in the long term, inventory costs at all times return to their true grasp: earnings.

For example, take a look at the chart under that reveals us the important thing drivers of inventory efficiency over varied lengths of time.

The column on the left reveals us the drivers over one yr. “A number of” (which suggests “investor sentiment”) is in crimson; it’s the dominant affect at 46%. Income progress (the premise for “earnings”) is in blue; it accounts for simply 29% of stock-price efficiency.

However see how this flips the additional out you go (the columns to the suitable).

Supply: Morgan Stanley / The Future Buyers

After 10 years, sentiment drives just 5% of stock performance.

For another angle on this, below is a chart dating to 1945 comparing the S&P 500’s price to its trailing 12-month operating earnings.

Notice how over the long-term, these two lines have an amazingly strong correlation. This underscores our point: In the long-run, earnings drive stock prices.

But also, you’ll see how the S&P’s price line (in green) bounces all around the S&P’s much smoother earnings line (in blue).

This is showing us how price – pushed and pulled by sentiment – soars and crashes… yet always returns to the earnings line.

Source: Investment Strategy Group, Bloomberg, S&P Global

So, where are we with this earnings/sentiment dance today?

In recent weeks, the stock market has been tanking largely due to the investor sentiment part of the equation

And this just prompted legendary investor Louis Navellier’s favorite economist, Ed Yardeni, to lower his S&P 500 forecast.

Yardeni has been one of Wall Street’s leading bulls in recent years – which has been the correct call. Today, he remains broadly bullish. To that end, he hasn’t changed his forecast for 2025 earnings, but he’s pulling back on his sentiment multiple.

From MarketWatch:

Yardeni is sticking with his view that S&P 500 companies will earn a combined $285 per share…

But he is blinking on the valuation multiple, now expecting a range of 18 to 20 instead of 18 to 22.

That takes Yardeni’s best-case scenario down to 6,400 from 7,000 (and also his year-end 2026 view down to 7,200 from 8,000). His “worst-case scenario” for the end of 2025 is now down to 5,800.

The good news is that Yardeni’s updated “worst-case scenario” still has the S&P climbing almost 4% from where it trades as I write.

This isn’t to say that Yardeni doesn’t recognize the potential for earnings to take a hit. Here he is, with a warning:

The latest batch of economic indicators released on Monday, Tuesday, and Wednesday supported our resilient economy scenario with subdued inflation.

Nevertheless, we can’t ignore the potential stagflationary impact of the policies that Trump 2.0 is currently implementing haphazardly.

But Goldman Sachs has, in fact, lowered its earnings forecast due to tariff wars

It’s not a drastic reduction, from $268 to $262. For perspective, the broad Wall Street consensus is $270.

Here’s MarketWatch explaining:

[The reduced earnings forecast is] in reaction to Goldman’s economists earlier this week lowering their GDP view on expectations of a 10-percentage-point tariff-rate increase.

The simple math is that every five-percentage-point increase in the tariff rate reduces S&P 500 earnings by 1% to 2%.

The new earnings forecast also took into account elevated uncertainty and tightening financial conditions.

Meanwhile, like Yardeni, Goldman also lowered its sentiment multiple. But again, not by much – from 21.5 to 20.6.

From Goldman:

The headwinds to equity valuations from a spike in uncertainty are typically relatively short lived.

However, an outlook for slower growth suggests lower valuations on a more sustained basis.

But here, too, Goldman sees stocks climbing from here to end of 2025, even after its reduced forecast. It puts the S&P at 6,200 by year-end, which is 11% higher.

So, if earnings are remaining relatively robust in these projections, then might this “sentiment” correction be healthy?

Yes.

At the end of last year, sentiment had reached bullish extremes. That type of enthusiasm is fun, but it’s flimsy and usually doesn’t last for too long.

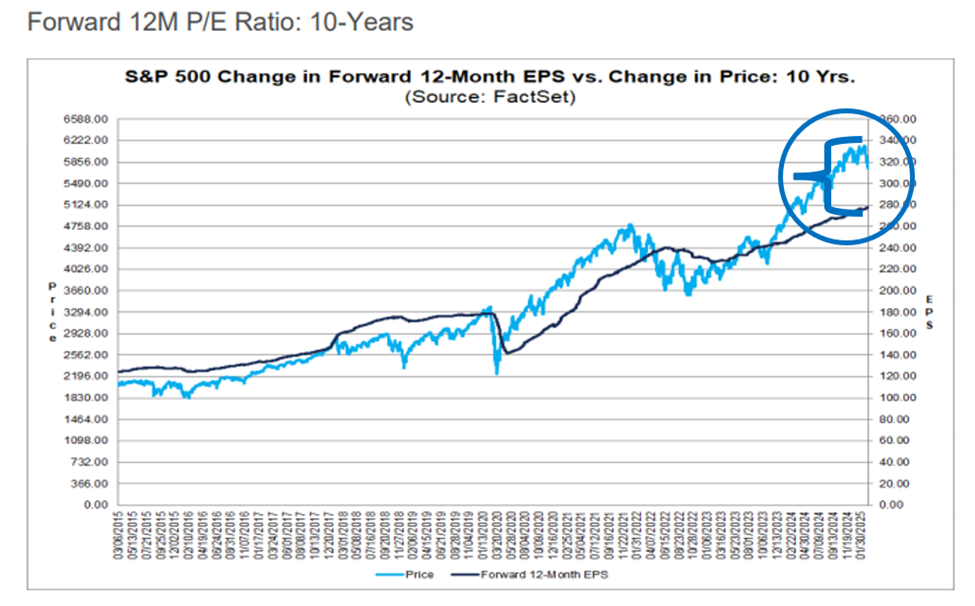

Below, we look at the S&P 500’s price in light blue compared with the change in the S&P’s forward 12-month earnings estimate dating to 2015.

Notice how price (in this case, our loose proxy for sentiment) had soared far higher than earnings estimates coming into 2025.

Source: FactSet

So far, given that earnings are holding up well, the pullback has reflected waning sentiment – but this has meant that the price/earnings divergence has narrowed to a more reasonable level.

If we want a long-term bull, this is good news. It’s like letting some air out of an overinflated balloon.

But will this pullback remain a relatively mild “sentiment” drawdown or intensify into a “sentiment + earnings” bear?

That’s the question.

After all, a “sentiment” pullback would mean we should be looking for great buying opportunities today. A “sentiment + earnings bear” would suggest a defensive posture.

Here are some numbers on the two scenarios…

MarketWatch found that when stocks fall 10% but don’t enter a recession, buying the S&P (after it has fallen 10%) has delivered gains six months later nearly 90% of the time (using data since 1980).

But if both sentiment and earnings take a hit, resulting in a bear market, the median S&P 500’s peak-to-trough pullback would be a 24% decline.

Let’s return to the question…

Do we need to be prepared for another massive leg lower in stocks due to an earnings collapse?

It doesn’t appear that way currently.

Here’s FactSet, which is the go-to earnings analytics group used by the pros:

For Q2 2025 through Q4 2025, analysts are calling for earnings growth rates of 9.7%, 12.1%, and 11.6%, respectively.

For CY 2025, analysts are predicting (year-over-year) earnings growth of 11.6%.

It’s going to be very hard to have a deep, sustained bear market with that kind of earnings growth.

Meanwhile, FactSet reports that while executives have been discussing tariffs on their earnings calls, they haven’t been mentioning “recession” with any great urgency.

Back to FactSet:

Through Document Search, FactSet searched for the term “recession” in the conference call transcripts of all the S&P 500 companies that conducted earnings conference calls from December 15 through March 6.

Of these companies, 13 cited the term “recession” during their earnings calls for the fourth quarter.

This number is well below the 5-year average of 80 and the 10-year average of 60.

In fact, this quarter marks the lowest number of S&P 500 companies citing “recession” on earnings calls for a quarter since Q1 2018.

But what about the recent GDP reduction that points toward a recession?

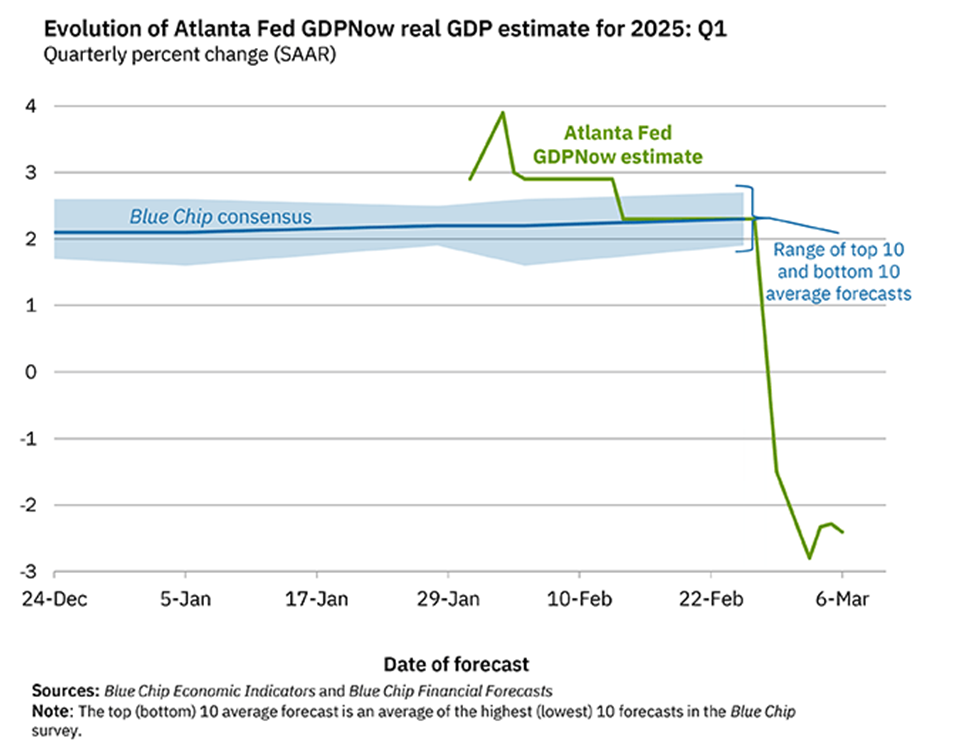

To make sure we’re all on the same page, the Atlanta Fed’s GDPNow Tool provides a “nowcast” of the official GDP estimate prior to its release by using a methodology similar to the one used by the U.S. Bureau of Economic Analysis.

As I write, it’s showing a steep contraction of -2.4%.

Source: Atlanta Fed

We need to take this with a big grain of salt.

To explain why, here’s Louis from Wednesday’s Flash Alert podcast in Breakthrough Stocks:

The info doesn’t assist us going right into a recession.

Now, I’ve talked about to you people that the commerce surpluses are ridiculous as a result of corporations had been dumping items on America.

The primary indication was the 34% surge in January. We’ll see what the February commerce quantity will probably be, however that would trigger unfavorable Gross Home Product (GDP).

Nonetheless, in accordance with the Institute of Provide Administration (ISM), manufacturing has been rising for 2 months in a row after contracting for 26 months, and companies really picked up.

The U.S. is a predominantly service-led financial system, so the information doesn’t assist the narrative that we’re going right into a recession.

Circling again to our concentrate on earnings, Louis is the proper particular person to chime in on at the moment’s theme of “sentiment” and “earnings”

In any case, as we highlighted in yesterday’s Digest, Louis’ total strategy to the market facilities on figuring out shares displaying elementary energy.

True to type, right here’s what Louis mentioned on Wednesday to his subscribers:

I wish to reassure you that earnings are working.

I additionally wish to reassure you that once we had this very sharp correction that analysts by no means minimize their estimates…

We’ll keep watch over every thing, and we’ll simply preserve you within the crème de la crème – the very best shares.

Talking of crème de la crème, a reminder that Louis simply flagged his prime quantum computing inventory. He believes it has 50X upside potential as quantum computing applied sciences hits the mainstream (there’s breaking information on this that we’ll function in Saturday’s Digest – be looking out).

Louis additionally pointed towards a key catalyst taking place this coming Thursday – Nvidia Corp.’s (NVDA) “Quantum Day.” Right here’s Louis:

Subsequent Thursday,I consider Nvidia will stake its declare within the quantum computing area. And when it does, this little-known prime choose might erupt in a single day.

Yesterday, I revealed everything you need to know about Q-Day – together with particulars on my No. 1 inventory choose that would explode within the wake of NVIDIA’s announcement.

To take a look at Louis’ full presentation, click here.

Coming full circle…

So, what are we to conclude from all this?

Right here’s the quick-and-dirty:

- Our present drawdown is basically “sentiment” pushed. At current, that provides the sting to this being a shopping for alternative

- Primarily based on present earnings forecasts, it’s unlikely we’ll devolve into an earnings recession, which might usher in a extra damaging bear market

- Nonetheless, tariff wars might change the calculus relying of their severity and period

- Specializing in the earnings energy of your particular shares is the easiest way to keep away from pointless stress – or kneejerk selections – in a market local weather reminiscent of this one.

We’ll preserve you up to date.

Have a great night,

Jeff Remsburg

{kind=link}