Government abstract

-

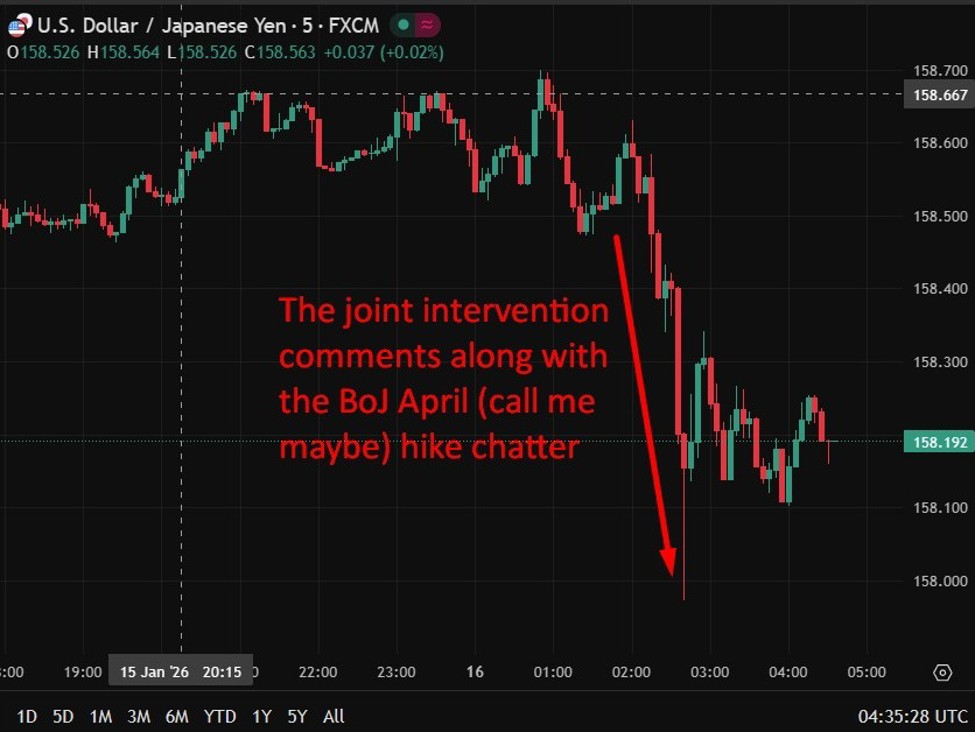

JPY outperformed, pushed by renewed FX intervention warnings and Reuters reporting that some BOJ policymakers see scope for an earlier price hike, with April in play

-

NZD edged greater after a powerful manufacturing PMI and additional moderation in meals costs supported the near-term progress and inflation outlook

-

US commerce coverage threat resurfaced, with the White Home flagging that AI chip tariffs have been solely a “section one” motion

-

ECB signalled price stability, however warned Fed coverage dangers may spill into world markets

-

Geopolitics cooled modestly, with Iran signalling restraint; oil ticked greater however safe-haven demand eased, weighing on gold

-

China moved to curb high-frequency buying and selling, slicing latency benefits by forcing servers out of change knowledge centres

The yen was the standout mover, surging after Japan’s finance minister stated foreign-exchange intervention stays an choice beneath the U.S.–Japan framework and that no measures, together with joint motion, are being dominated out. The warning in opposition to extreme or disorderly strikes delivered a right away market impression. The transfer gathered additional momentum after a Reuters report stated some Financial institution of Japan policymakers see scope to lift rates of interest before markets anticipate, with April rising as a dwell chance if weak-yen-driven inflation dangers proceed to broaden. The report underscored rising inside concern that yen depreciation may encourage wider worth pass-through, complicating the BOJ’s assumption that cost-push pressures will fade easily. Yen crosses fell, with USD/JPY briefly slipping under 158.00 earlier than discovering its ft.

That stated, the yen’s underperformance earlier this month has been exacerbated by political dynamics, with expectations that an election victory for Prime Minister Sanae Takaichi would give her a powerful mandate for expansionary fiscal coverage, an element that has saved structural stress on the foreign money regardless of rising intervention rhetoric. A sustained restoration for the yen is tough to know on this setting.

–

Earlier within the session:

In New Zealand, knowledge movement remained supportive. The manufacturing PMI jumped to 56.1 in December, the strongest studying since 2021, with all sub-indices increasing and new orders main the acquire. BNZ flagged upside threat to This fall GDP and stable momentum into early 2026. That was adopted by a softer Meals Value Index, which fell 0.3% m/m in December after a -0.4% print in November. Whereas meals costs stay up 4% y/y, the sequential declines are an encouraging sign for the Reserve Financial institution of New Zealand, serving to the kiwi observe modestly greater on the session.

In the US, commerce coverage uncertainty returned to the fore. After imposing a 25% tariff on a slender set of superior AI chips earlier this week, a White Home official stated the measures ought to be seen as a “section one” motion, with additional bulletins potential relying on negotiations with overseas governments and corporations.

In Europe, ECB Chief Economist Philip Lane reiterated that there isn’t a near-term price debate if the baseline outlook holds, however warned that U.S.-origin shocks — together with any departure by the Federal Reserve from its mandate — may destabilise world monetary circumstances and power a reassessment in Europe.

On the geopolitical entrance, studies {that a} U.S. plane provider is shifting to the Center East have been largely seen as stale, having circulated earlier within the week. Iran’s deputy UN envoy stated Tehran seeks neither escalation nor confrontation, although warned any aggression would draw a powerful and lawful response. Oil opened just a few cents greater, whereas gold slipped as easing geopolitical rigidity lowered safe-haven demand.

Lastly, China moved to rein in high-frequency buying and selling, forcing servers out of change knowledge centres in Shanghai and Guangzhou — a step that can scale back latency benefits for each home and world buying and selling companies.

Asia-Pac

shares:

- Japan

(Nikkei 225) -0.05% - Hong

Kong (Cling Seng) -0.27% - Shanghai

Composite -0.22% - Australia

(S&P/ASX 200) +0.42%

—

Have a fantastic weekend, see you all on Monday for impactful China knowledge on the agenda!

{kind=link}