China’s companies sector stays in enlargement however is slowing, with home demand supporting development whereas weak exports, falling employment and worth discounting level to softer underlying momentum.

Abstract:

- China Providers PMI eases to 52.1 (prev 56.7), nonetheless expansionary

- Progress slows sharply from February’s 33-month excessive

- Home demand stays the important thing driver of exercise

- New export orders slip again into contraction

- Employment falls for a second straight month

- Value pressures stay modest, permitting companies to chop costs

- Enterprise confidence stays optimistic regardless of softer momentum

- Composite PMI additionally slows however stays in development territory

Earlier this week:

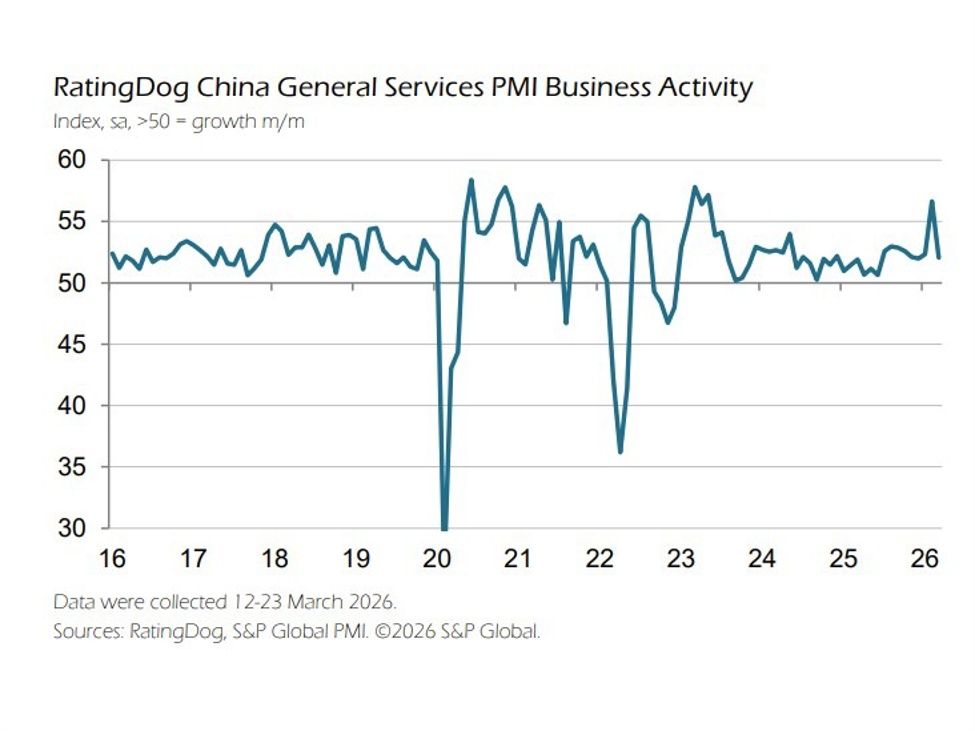

China’s service sector continued to broaden in March, although the tempo of development moderated notably following February’s sturdy efficiency, with home demand offering the first assist amid softer exterior circumstances.

The RatingDog China Common Providers PMI got here in at 52.1, down from February’s 33-month excessive of 56.7, signalling a slower however nonetheless strong enlargement in exercise. The sector has now remained in development territory for over three years, reflecting a sustained restoration pattern.

Incoming new enterprise continued to rise, extending the present enlargement sequence to 39 consecutive months. Nevertheless, the tempo of development eased to its slowest since April 2025, suggesting a lack of momentum after the earlier month’s surge. Survey respondents attributed new work primarily to stronger home demand, together with improved buyer bases and new venture exercise.

In distinction, exterior demand weakened. New export orders slipped again into contraction territory after development earlier within the 12 months, highlighting ongoing fragility in international demand circumstances.

Regardless of continued will increase in new enterprise and backlogs of labor, companies diminished staffing ranges for a second consecutive month. Job shedding was modest however marked the quickest tempo in six months, reflecting price management measures, restructuring and the non-replacement of departing employees.

On the pricing entrance, the report pointed to a notably completely different dynamic in contrast with different areas. Enter prices rose solely modestly and remained beneath long-run averages, permitting companies to decrease their promoting costs to assist demand. Output expenses fell for the third time in 4 months, signalling aggressive pressures and subdued pricing energy.

Wanting forward, enterprise sentiment remained optimistic general, supported by expectations of improved market circumstances and enlargement plans. Nevertheless, the mix of slowing development, weak exterior demand and ongoing employment contraction suggests a extra uneven restoration path regardless of continued enlargement.

{kind=link}