UPCOMING

EVENTS:

- Monday: German IFO.

- Tuesday: US Shopper Confidence.

- Wednesday: Australia Month-to-month CPI.

- Thursday: Switzerland This fall GDP, US Sturdy Items Orders, US

This fall GDP (2nd estimate), US Jobless Claims. - Friday: Tokyo CPI, France CPI, Germany CPI, Canada GDP,

US PCE.

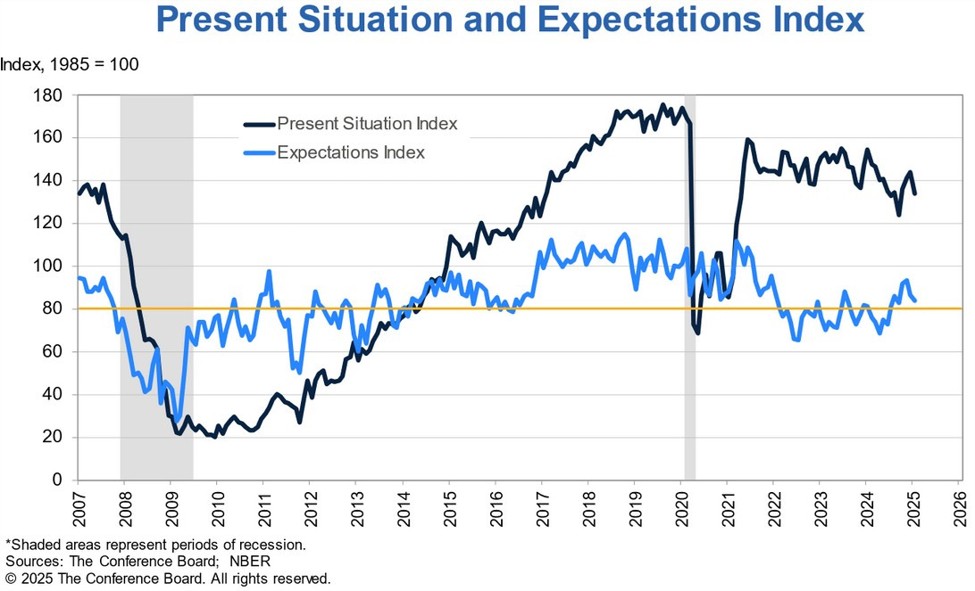

Tuesday

The US Shopper

Confidence is anticipated at 103.0 vs. 104.1 prior. The final report confirmed Shopper Confidence dropping for the second

consecutive month though it remained within the vary created since 2022.

Dana M. Peterson,

Chief Economist at The Convention Board mentioned: “all 5 elements of the Index

deteriorated however customers’ assessments of the current state of affairs skilled

the biggest decline. Notably, views of present labour market situations fell

for the primary time since September, whereas assessments of enterprise situations

weakened for the second month in a row.”

“In the meantime,

customers had been additionally much less optimistic about future enterprise situations and, to a

lesser extent, earnings. The return of pessimism about future employment

prospects seen in December was confirmed in January.”

US Shopper Confidence

Wednesday

The Australian

Month-to-month CPI Y/Y is anticipated at 2.5% vs. 2.5% prior. Inflation has been

step by step falling in direction of the RBA’s goal with the most recent Australian This fall CPI exhibiting underlying inflation inside

the 2-3% goal band on a 6-month annualised foundation.

As a reminder, the

RBA lower rates of interest by 25 bps as anticipated final week nevertheless it was

accompanied by a extra hawkish than anticipated steerage. We’ve additionally obtained the Australian Employment report and as soon as

once more the information confirmed a strong labour market.

Australia Month-to-month CPI YoY

Thursday

The US Jobless

Claims proceed to be one of the crucial necessary releases to comply with each week

because it’s a timelier indicator on the state of the labour market.

Preliminary Claims

stay contained in the 200K-260K vary created since 2022, whereas Persevering with Claims

proceed to hover round cycle highs though we’ve seen some easing lately.

This week Preliminary

Claims are anticipated at 220K vs. 219K prior, whereas there’s no consensus on the

time of writing for Persevering with Claims though final week we noticed a rise to

1869K vs. 1845K prior.

US Jobless Claims

Friday

The Tokyo Core CPI

Y/Y is anticipated at 2.3% vs. 2.5% prior. The JPY strengthened lately on extra

hawkish feedback from BoJ officers, and strong wage progress and inflation information.

Final Friday, the JPY obtained one other increase on some risk-off strikes triggered by the

US shares selloff following the weaker than anticipated US PMIs and long-term

inflation expectations within the UMich survey leaping to a brand new 30-year excessive.

Tokyo Core CPI YoY

The US PCE Y/Y is

anticipated at 2.5% vs. 2.6% prior, whereas the M/M measure is seen at 0.3% vs. 0.3%

prior. The Core PCE Y/Y is anticipated at 2.6% vs. 2.8% prior, whereas the M/M

determine is seen at 0.3% vs. 0.2% prior.

Forecasters can reliably

estimate the PCE as soon as the CPI and PPI are out, so the market already is aware of what

to count on. Due to this fact, except we see a deviation from the anticipated numbers, it

shouldn’t have an effect on the present market’s pricing.

US Core PCE YoY

{kind=link}