Knowledge is right here:

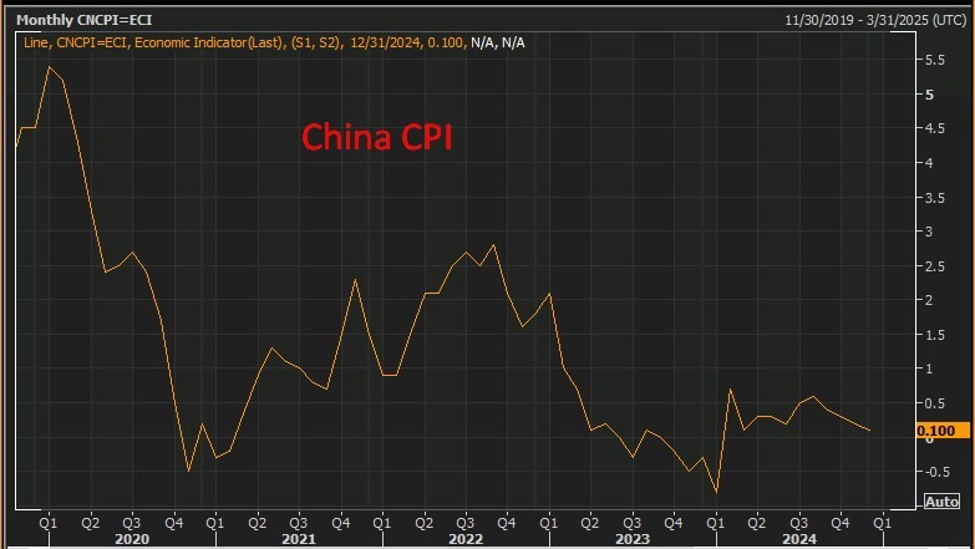

- China December CPI +0.1% y/y (anticipated +0.1%, prior +0.2%)

Recap (abstract of a Reuters report):

-

Client Value Index:

- China’s CPI rose by 0.2% in 2024, matching the earlier yr’s progress and falling properly under the three% goal.

- December CPI elevated by 0.1% year-on-year, slowing from 0.2% in November and marking the weakest tempo since April.

- Core inflation, excluding meals and gas, edged as much as 0.4% in December, the very best in 5 months.

-

Producer Value Index:

- Manufacturing unit-gate costs declined for the twenty seventh consecutive month, with the PPI falling 2.3% in December year-on-year, an enchancment from November’s 2.5% decline.

-

Financial Challenges:

- Persistent weak home demand is pushed by:

- Job insecurity.

- A protracted housing market downturn.

- Excessive debt ranges.

- Uncertainty over U.S. commerce insurance policies beneath President-elect Donald Trump.

- Discounting is widespread throughout retail sectors, together with objects like bubble tea and luxurious items, whereas customers more and more lease as a substitute of buying discretionary objects.

- Persistent weak home demand is pushed by:

-

Stimulus Measures:

- Coverage stimulus has offered non permanent help to demand and costs, however analysts anticipate its results to fade, with inflation prone to weaken later in 2025.

- Beijing has ramped up fiscal measures, together with:

- A file $411 billion in particular treasury bond insurance coverage.

- Plans for substantial funding from ultra-long treasury bonds in 2025.

- $41 billion allotted for tools upgrades and shopper items trade-ins, together with autos.

-

Analyst Outlook:

- Economists level to persistent deflationary pressures, with inflation restoration tied to the effectiveness of fiscal insurance policies.

- The property sector downturn continues to tug on shopper confidence.

- Whereas the World Financial institution has upgraded China’s progress forecast for 2024–2025, subdued family and enterprise sentiment stays a priority.

CPI:

This text was written by Eamonn Sheridan at www.forexlive.com.

Source link

{kind=link}