An Obamacare signal at a Miami insurance coverage company on Nov. 12, 2025.

Joe Raedle | Getty Pictures

The White Home on Thursday reiterated its support for sending funds on to households to cover health-care costs, an concept President Donald Trump has championed for months.

Nevertheless, well being coverage consultants reached by CNBC mentioned they had been skeptical of the proposal.

“I do suppose it is a unhealthy concept,” mentioned Gerard Anderson, a professor of well being coverage and administration on the Johns Hopkins Bloomberg College of Public Well being.

The coverage was a part of a broad outline of a health-care plan that the White Home mentioned would decrease drug costs and insurance coverage premiums. In a video unveiling the framework, dubbed “The Nice Healthcare Plan,” Trump referred to as on Congress to swiftly codify it into regulation.

Trump has proven enthusiasm for sending direct funds in different contexts throughout his second time period, floating concepts together with tariff dividend checks.

It is arduous to evaluate the precise influence of direct health-care funds, consultants mentioned, for the reason that White Home framework lacked key particulars comparable to who could be eligible, the quantity customers would possibly obtain and the way the cash may very well be spent.

At a excessive stage, it would not seem the proposal would grant the identical stage of economic help for well being care that buyers at the moment obtain, which might probably lead many to drop their insurance and trigger premiums to rise for remaining enrollees, Anderson mentioned.

There would additionally need to be robust guardrails in place to dictate how individuals might spend their health-care funds, mentioned Nick Fabrizio, a well being coverage professional and affiliate instructing professor at Cornell College’s Jeb E. Brooks College of Public Coverage.

“I really feel very strongly that should you give individuals cash, they may spend it on issues apart from well being care except it is like a voucher,” Fabrizio mentioned.

Trump’s general framework, which requires insurance policies like higher worth transparency within the medical ecosystem, might achieve decreasing well being prices, Fabrizio mentioned.

Trump framework comes amid ACA subsidy debate

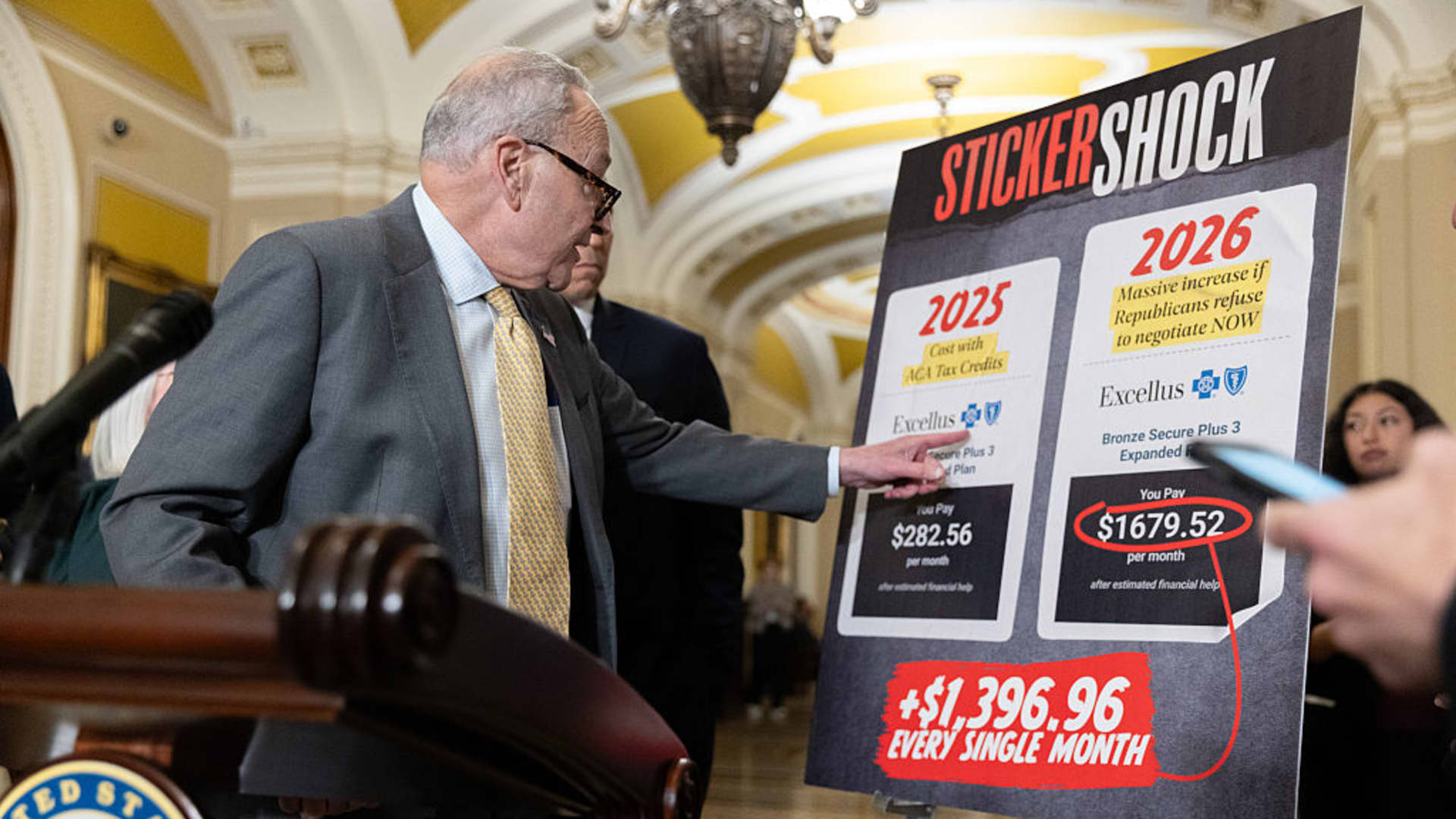

Senate Minority Chief Chuck Schumer, D-NY, speaks at a press convention with different members of Senate Democratic management following a coverage luncheon on the Capitol on Oct. 15, 2025.

Anadolu | Getty Pictures

The framework comes as Congress is debating whether or not to extend enhanced subsidies that lower insurance premiums for hundreds of thousands of Reasonably priced Care Act market enrollees, and it could complicate a bipartisan effort underway to resume them.

These enhanced subsidies, in place since 2021, expired on the finish of final 12 months. KFF, a nonpartisan well being coverage analysis group, estimated the lapse would trigger premiums to soar greater than twofold for the typical recipient.

With out the enhancement, a baseline of subsidies often called premium tax credit continues to be in place for ACA enrollees.

Shoppers can choose to obtain these premium tax credit in one in every of two methods: in a lump sum throughout tax season, or by way of an instantaneous discount in month-to-month insurance coverage premiums.

Within the latter situation, by far the most well-liked, the federal authorities sends a shopper’s subsidy to their insurer, which then lowers the patron’s upfront premium.

Trump’s well being framework referred to as for an finish to “billions in further taxpayer-funded subsidy funds” and as an alternative supported sending that cash “on to eligible People to permit them to purchase the medical health insurance of their alternative.”

It is unclear how such a plan would work, consultants mentioned.

Trump and a few congressional Republicans had beforehand supported the concept of repealing some or all ACA subsidies and changing them with contributions to well being financial savings accounts or one thing comparable, wrote Larry Levitt and Cynthia Cox of KFF. A well being financial savings account is a tax-advantaged account geared to medical expenses.

A White Home official mentioned Thursday that buyers outdoors the ACA market would additionally qualify for direct funds.

Whereas HSAs can be utilized to cowl sure medical bills, customers cannot at the moment use them to pay insurance coverage premiums — and solely customers who’re enrolled in a qualifying high-deductible medical health insurance plan can make a contribution to such an account, consultants mentioned.

“You’d have hurdles getting individuals by way of the door” and into an insurance coverage plan if that HSA prohibition in opposition to premium funds had been to stay, mentioned Matt McGough, an Reasonably priced Care Act coverage analyst at KFF. “It is actually not going to alleviate numerous the [financial] burden for these individuals.

“The satan is basically within the particulars right here,” he mentioned.

Quantity is a key lacking element

The direct fee quantity and the extent to which any remaining premium tax credit could be scaled again are different necessary, unknown particulars, consultants mentioned.

If the quantity weren’t giant sufficient, then youthful, more healthy individuals would usually be those to drop their protection — leaving older, sicker enrollees behind, Anderson mentioned. Insurers would increase premiums for the remaining insured to compensate for that danger, since older, sicker enrollees usually require extra care, he mentioned.

Laws unveiled in December by Sens. Mike Crapo, R-Idaho, chair of the Senate Finance Committee, and Invoice Cassidy, R-La., chair of the Senate Well being, Training, Labor and Pensions Committee, would provide an annual HSA contribution of $1,000 for people ages 18 to 49 or $1,500 for people ages 50 to 64.

That sum “actually pales compared” to what many enrollees, particularly these ages 50 to 64, had obtained from enhanced ACA subsidies, McGough mentioned.

For instance, the typical middle-income 60-year-old incomes virtually $63,000 a 12 months is now not eligible for ACA subsidies, and is on the hook for the complete, unsubsidized insurance coverage premium in 2026 — about $15,000, in response to a KFF analysis. In 2025, this similar particular person was eligible for an ACA premium subsidy of about $7,300.

Premium tax credit score quantities fluctuate drastically from individual to individual, primarily based on age, earnings and geography.

{kind=link}