For the previous few weeks, buyers have been trapped in a “fog of struggle.”

They’ve been fixated on the headlines, worrying about oil costs, inflation and the implications for future charge cuts.

That’s comprehensible.

The excellent news is that the first-quarter earnings season has arrived simply in time.

As a result of after weeks of tension, rumor and geopolitical noise, buyers lastly have one thing extra concrete to give attention to: numbers, steering and tangible proof about what is absolutely taking place within the financial system.

That’s the reason the primary wave of financial institution earnings issues.

Now, longtime readers know I’ve by no means been an enormous fan of banks.

I was a banking regulator, and I noticed firsthand how versatile their monetary reporting may be.

That have scarred me for all times. It is among the largest causes I nonetheless method financial institution earnings with a wholesome dose of skepticism.

So no, I’m not immediately pounding the desk on huge banks.

However as a result of banks are likely to report first, their earnings nonetheless supply an early learn in the marketplace and the financial system.

And this week’s outcomes gave us a helpful message.

They advised us that elements of the financial system are holding up higher than many feared. However there are nonetheless some indicators that warrant warning.

So immediately, let’s have a look at what three huge financial institution earnings studies are actually telling us.

Then I’ll present you why that issues for what comes subsequent – and the place I consider the true alternative is beginning to emerge.

The Goldman Sachs Group, Inc.

Let’s begin with The Goldman Sachs Group, Inc. (GS), which kicked off earnings season on Monday morning.

The agency introduced a 19% year-over-year enhance in earnings, to $5.6 billion, or $17.55 per share. Income rose 14% to $17.23 billion.

Each earnings and income beat analysts’ expectations.

Wanting nearer, Goldman posted file equities buying and selling income of $5.33 billion, a 27% enhance. Funding banking charges additionally rose 48% to $2.84 billion. Each numbers had been above expectations.

Regardless of these robust outcomes, Goldman Sachs shares dipped 2% following the report, suggesting buyers could also be questioning the sustainability of this progress.

That’s as a result of Goldman’s power got here from buying and selling and funding banking, areas that have a tendency to learn when markets get extra lively.

JPMorgan Chase & Co.

Subsequent, we’ve JPMorgan Chase & Co. (JPM).

It reported robust outcomes, with earnings growing 13% to $16.5 billion, or $5.94 per share, and income rose 10% to $50.54 billion. Each topped analysts’ estimates.

Digging additional into the report, mounted revenue buying and selling income rose 21% to $7.08 billion. Funding banking charges elevated 28% to $2.88 billion.

JPMorgan additionally put aside much less cash for mortgage losses, indicating that debtors are paying again their loans and suggesting that customers are extra financially secure. The corporate, nonetheless, lowered its 2026 internet curiosity revenue steering for 2026, from $104.5 billion to about $103 billion.

CEO Jamie Dimon additionally struck a cautious tone, noting that whereas the U.S. financial system stays resilient, there are nonetheless “important uncertainties” forward, together with geopolitical dangers, inflation pressures and elevated asset costs.

Now, I’ve joked earlier than that Jamie Dimon is a little bit of a “fear wart,” and I believe that’s the case right here once more. Shares of JPMorgan fell about 2%, regardless of the outcomes and Dimon’s cautious outlook, which appeared to weigh on investor sentiment.

Financial institution of America Company

Lastly, we flip to Financial institution of America Company (BAC), which reported Wednesday morning.

Financial institution of America reported its highest earnings per share in almost 20 years, rising 17% to $1.11.

Income rose 7.2% to $30.43 billion, because of rising internet curiosity revenue, larger buying and selling income and funding banking charges.

However in contrast to the opposite banks, one other issue contributed to its progress.

Financial institution of America noticed power in its shopper enterprise, with strong spending and secure credit score high quality.

CEO Brian Moynihan emphasised that shopper spending remained strong and credit score high quality stayed secure, highlighting the resilience of the U.S. shopper regardless of ongoing uncertainty.

Financial institution of America shares rose about 2% following the report.

What Inventory Grader Has to Say

Whereas every of the outcomes appears to be like strong on the floor, the larger query is that if they’re good buys proper now.

Let’s see what my Stock Grader system (subscription required) has to say about these huge banks…

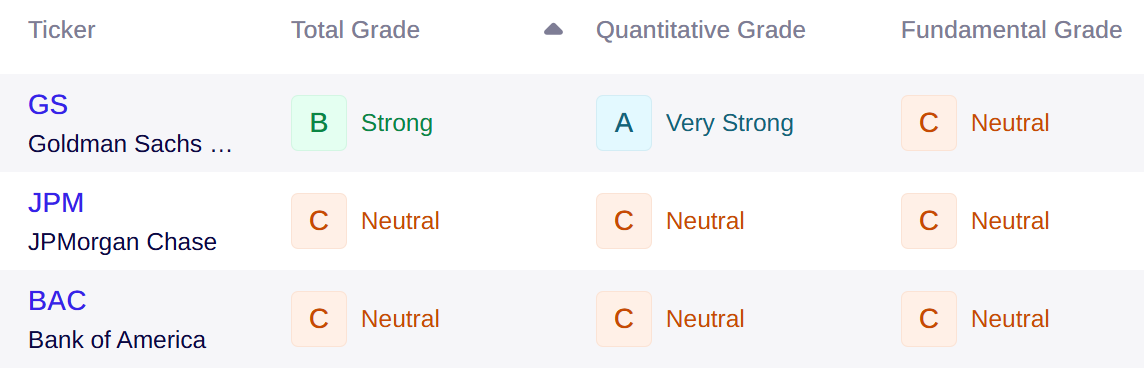

Goldman Sachs earns a Whole Grade of B, making it “Robust.”

Nevertheless, JPMorgan and Financial institution of America each have a Whole Grade of C, making them “Impartial.”

I also needs to add that every one three have basic grades that aren’t precisely inspiring. So, whereas these banks did put up strong numbers, they don’t stand out. And so they’re not the type of essentially superior shares I’m in search of.

Backside line: I wouldn’t contemplate them good buys proper now.

What These Earnings Are Actually Telling Us

If you step again and have a look at these studies collectively, a transparent sample emerges.

The excellent news is that the financial system is holding up higher than many feared.

However a whole lot of the power we noticed got here from buying and selling and funding banking companies that are likely to do nicely when markets get noisy.

That type of power can produce an excellent quarter.

It doesn’t all the time produce sturdy market management.

And that’s the distinction buyers want to bear in mind proper now.

I’m not in search of shares benefiting from short-term volatility. I’m in search of shares with the type of long-term demand, earnings momentum and basic power that may preserve outperforming from right here.

That’s precisely why instruments like Inventory Grader matter a lot in a market like this.

They assist separate common shares from the actually superior ones.

And more and more, they’re pointing me towards a selected group of corporations benefiting from what I name the “Hidden Crash.”

Whereas many buyers stay caught in crowded, slow-growth areas of the market, these corporations are tied to a really completely different pattern – one pushed by actual demand, not simply market exercise.

In a recent presentation, I defined what the Hidden Crash is and how one can get forward of it earlier than the remainder of the market catches on.

Sincerely,

Louis Navellier

Editor, Market 360

P.S. On April 22 at 10 a.m. Jap, TradeSmith CEO Keith Kaplan is revealing how his AI Alerts system identifies high-probability trades earlier than they occur. However you don’t have to attend till then – you can begin exploring the system now and see the way it analyzes shares in actual time. Reserve your spot here and get access.

{kind=link}